Introduction and Overview

In our commentary published on December 17 th , 2024, we cautioned against market over-optimism across a range of asset classes, including public equity and credit markets. From the end of 2024 until early April 2025, we maintained our short bias by allocating the proceeds from exiting certain positions to cash and cash equivalents and selective credit shorts. In response to developments over the past few weeks, we have adjusted our positioning to a neutral-to-long bias, while remaining flexible amid continued market volatility.

Search of a New Goldilocks

The new US administration is in search of a “new Goldilocks” situation, in which the GDP-reducing effects of cuts in government spending would be offset by a shrinking trade deficit. Over the past 3 years, we have pointed to various imbalances in the US fiscal picture and remained skeptical about whether growth in the US economy was sustainable or not, especially as it was fueled by government spending levels which yielded federal deficits as large as 7% of GDP. We have previously criticized the Federal Reserve’s decision to cut rates prematurely while inflationary pressures persisted through much of 2024, leaving inflation elevated. However, we have been encouraged by the backbone that the Fed has exhibited over the past 6 months. Based on the announcements from the new administration, we believe that their policy mix is in search of a new equilibrium with the dual aims of lowering inflation and rebalancing the economy.

Potential Impacts of New Administration’s Policy Policy Mechanism GDP Inflation Employment Deficit Rates

Creates incentive for Likely Tariffs Higher Higher Lower Mixed production to move to US Increase

Reduces government

[See the PDF for the complete table referenced in this section.]

Ambitious Plans for Rebalancing the US Economy

The current administration is embarking on an ambitious mission to rebalance the economy, with the goal of lowering the deficits, while keeping inflation low and spurring economic growth. However, each policy on its own may not necessarily align with all of the objectives (Table 1), which creates significant execution risk for the administration’s policies. Take the tariff policy, for example, which not only introduces the possibility for both benefits and costs but also could have a mixed impact on interest rates and increase the likelihood of execution risk. For starters, tariffs could result in higher prices in domestic (US) markets, but it is also possible that retaliatory measures, or a general slowdown in the ex-US world economy, would result in lower energy and food prices in the US. We are already seeing some evidence of deflation in energy prices and it is worth noting that Chinese counter-measures during the first Trump administration pushed food prices lower in the US. Moreover, by generating new revenues for the government, tariffs could reduce the amount of long-term debt issued by the Federal government, hence lowering treasury supply and pushing rates lower. At the same time, the one-off impact of tariff policy could push inflation higher and leave short-term interest rates elevated. The key risk of this policy—perhaps more than others—lies in its execution. With the outcome of trade negotiations uncertain, following through will require nerves of steel.

Tariff Revenues and Spending Cuts Aim to Reduce the Deficit to Sustainable Levels

We expect the administration to try to lower the deficit from 7-8% of GDP during the Biden/Yellen era to a more sustainable level of 3-4% of GDP by the end of its term. Their unofficial plan relies on both raising revenues from tariffs and cutting government spending. Throughout the campaign, and in their first months in office, administration officials have talked about raising $1trn annually from tariffs and cutting $1trn of government spending. Though we are skeptical about the magnitude of the numbers, we believe the new administration’s actions thus far indicate that both initiatives are headed in the right direction. Even if reaching 50% of its stated goal in each objective, this policy mix could reduce the deficit by at least $1trn, bringing it down to approximately 4% of GDP.

Controversial Call: Tariffs Could Boost the GDP in the Long Term

I recently appeared on a brief segment of Bloomberg Surveillance with Tom Keene to discuss how tariffs, if executed correctly, could possibly help drive economic growth in the US via an increase in GDP. All things being equal, GDP measures production (rather than consumption), and tariffs could increase domestic production through two main mechanisms in GDP: 1Decline in Trade Deficit 2Increase in (Domestic) Investments

Afterall, Gross Domestic Product (GDP) is commonly expressed using the simplified formula:

GDP = C + I + G + (X − M)

Where:

C = Consumption; I = Investment; G = Government Spending; X = Exports; M = Imports and the term (X−M) represents net exports, i.e., trade balance.

We will continue to discuss the administration’s policies and their effects in future commentaries as their impact becomes evident across the economy.

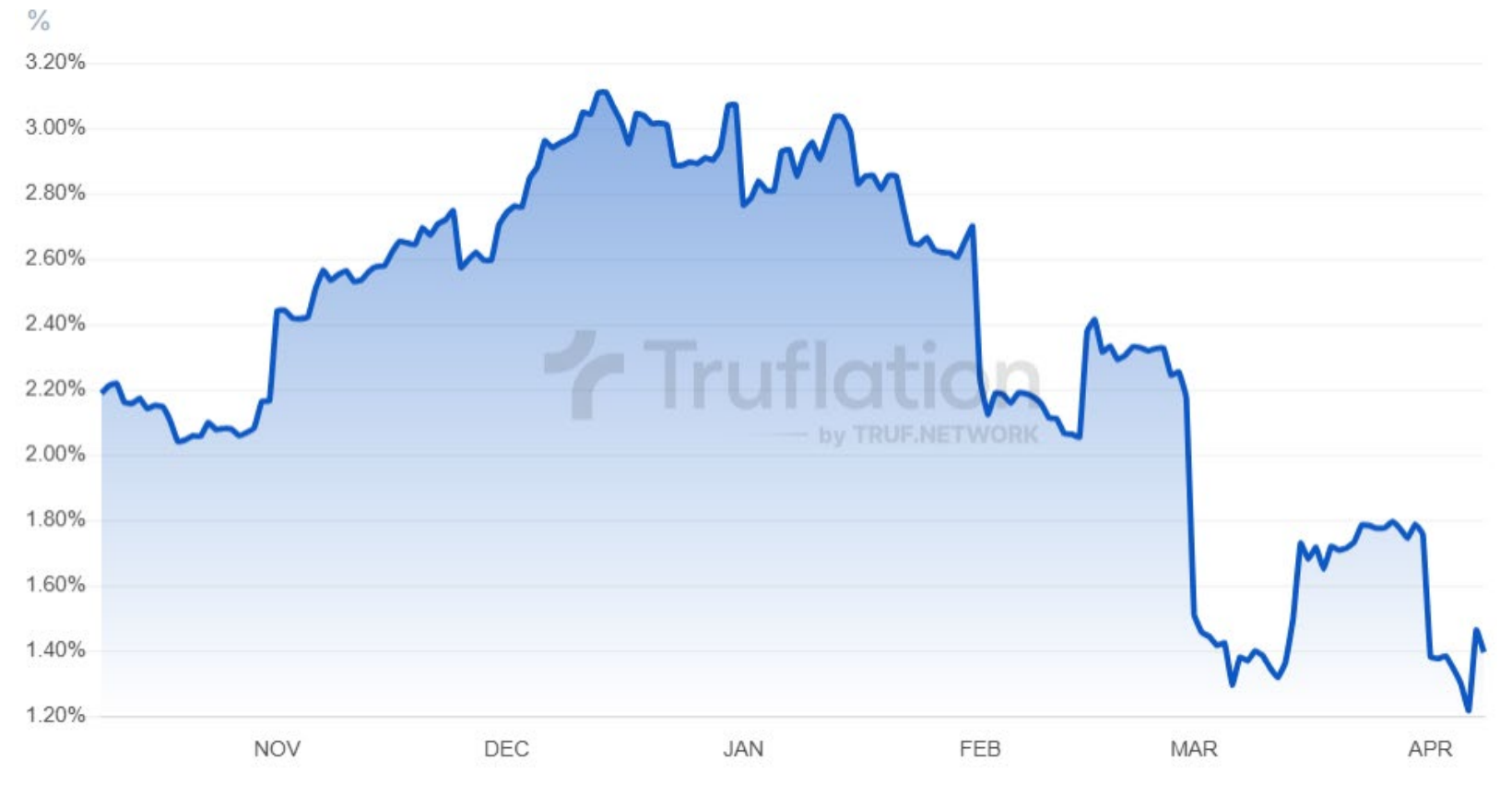

Inflation Has Fallen and Remains Subdued Early in the Administration’s Term

Our overview of real-time CPI data from Truflation (Figure 1) shows that inflation has shifted lower in March and remains low (below 2%). We will be keenly watching this indicator over the next few weeks to see how the impacts of tariffs are filtering through:

Opportunity Set

At the time of writing this report, we are excited about the opportunity set currently being presented to us. After two years of relentless spread tightening and leveraging the rally to exit a few of our positions, we are participating in a marketplace with wider spreads and renewed value in both liquid and private debt markets. Even the most enthusiastic supporters of the new administration would have to concede that it is reasonable to anticipate persistent uncertainty. With volatility as its trusty companion, we expect this continued uncertainty will create a stream of unique opportunities for Monachil.

Disclosures

The information contained in this document is for informational purposes only and should not be considered investment advice. This document does not constitute an offer to sell, a solicitation of an offer to buy, or a recommendation for any security or investment strategy.

Past performance is not indicative of future results. All investments carry risk, including the possible loss of principal. The views expressed herein are those of the author as of the date of publication and are subject to change without notice.

Forward-looking statements are based on current expectations and assumptions, which are subject to risks and uncertainties. Actual results may differ materially from those anticipated.

Monachil Capital Partners LP is a private investment firm. Investment opportunities described herein may be available only to qualified purchasers as defined under the Investment Company Act of 1940.