Introduction and Overview

Welcome to our October 2024 monthly report. As is our practice in these commentaries, we aim to highlight topical matters and assess their potential impact on financial markets. Since our previous letter, in which we highlighted emerging signs of stress in the treasury repo market and critiqued the Fed ’s decision to cut rates, yields have widened significantly. Compared to the pre-Fed meeting levels, both the 10-year and 2-year rates have increased by as much as 50 basis points. This pronounced movement has implications for the credit and fixed-income markets, prompting us to continue our examination of the dynamics in the treasury markets. Our findings indicate that US households and leveraged buyers, including hedge funds, are now the primary sources of incremental demand for US Treasuries, effectively absorbing the increased volume. Given the profile of these buyers, this shift in demand is likely to introduce increased volatility in other asset classes, such as equities and credit.

Widening Treasury Yields: Another Indicator of Potential Stress in Credit Markets

The recent widening of Treasury yields, which we believe is primarily supply-driven, has several implications for the credit markets. What raises concern for us is not the absolute level of rates – after all, a 10-year yield of 3.7% versus 4.2% would not materially impact short-term market dynamics – but rather the speed at which these rates have increased. The velocity of this movement suggests structural challenges and imbalances within the market. These imbalances are likely to persist, potentially driving rates even higher, which would create challenges for both corporations and consumers. Higher Treasury yields will increase borrowing costs for both corporations and households, as pricing in the corporate bond market and the mortgage market is closely tied to Treasury yields. For corporations, elevated borrowing costs could lead to lower profitability in future years. Additionally, refinancing may become more difficult for heavily indebted companies, pushing some closer to insolvency.

Impact of Higher Rates on the Housing Market and Existing Home Sale Volumes Has Been Profound

The impact of higher Treasury yields on households, particularly regarding mortgage rates, is significant. Increased rates make consumers more price-sensitive when considering home purchases, and we are already observing these effects in both new and existing home sales. Home sale volumes appear bifurcated. Recent US Department of Housing and Urban Development data indicates that new home sales settled at 738,000 units for the month of September, reflecting a slight month-over-month increase and relative stability over the past three years. In contrast, National Associations of Realtors data

shows that existing home sales dropped by 40% from 6.4 million units in January 2022 to 3.8 million units in September 2024 (both figures annualized). The rise in yields is likely to exert further pressure on the existing home sales market, dampening activity even more.

Treasury and Rates Market: Abundant Supply of Treasuries with Limited Capacity to Absorb

Readers familiar with our analysis will recognize our focus on the persistent increase in Treasury supply in recent years, driven by budget deficits and growing fiscal pressures. On October 8th, the CBO released its monthly budget review, detailing the full budget deficit figures for fiscal year 2024 (October 2023 to September 2024). The reported deficit stands at $1.8 trillion, approximately 7% of GDP. Considering the impact of the Fed ’s balance sheet reduction, Treasury supply has been increasing at a rate of $2-2.5 trillion annually over the past 3 years.

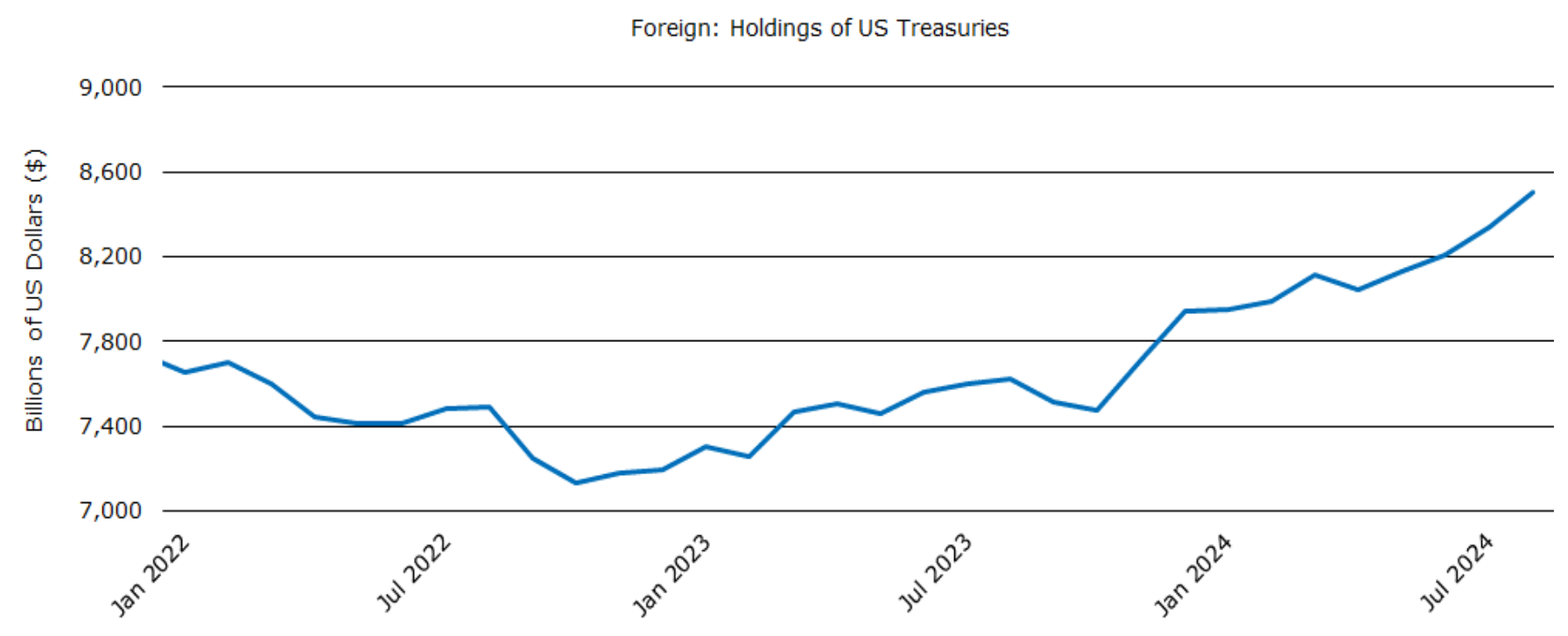

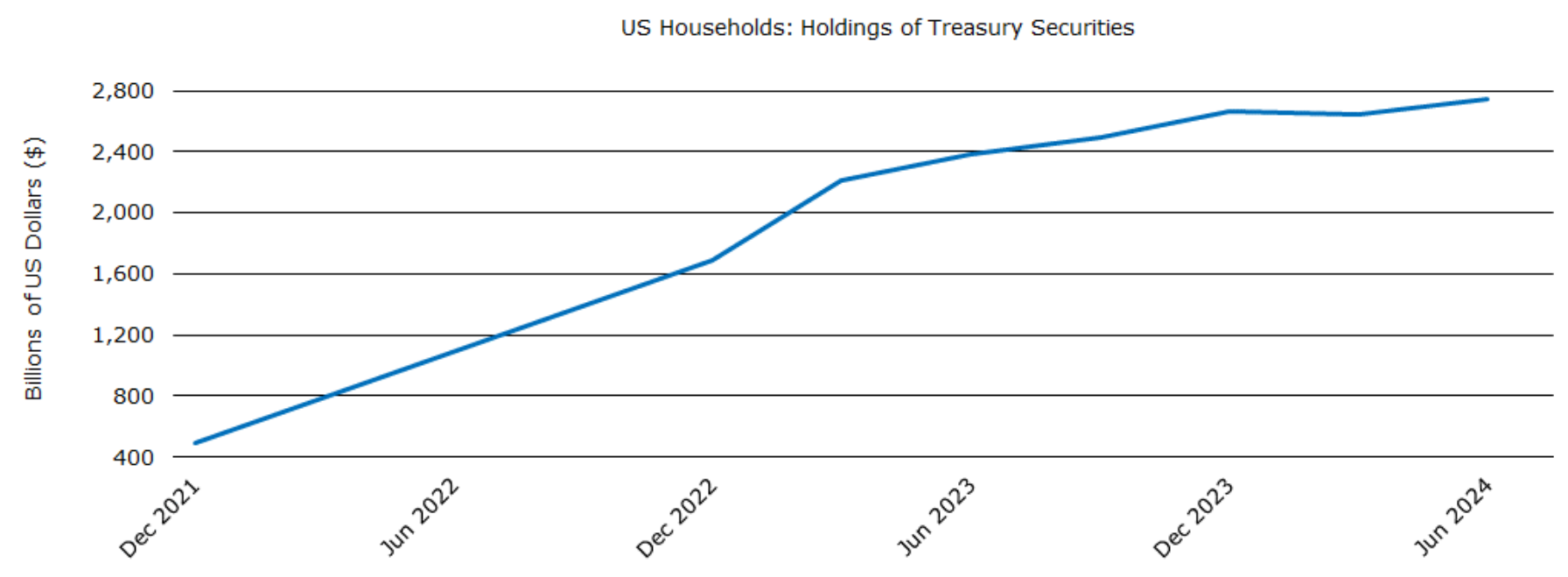

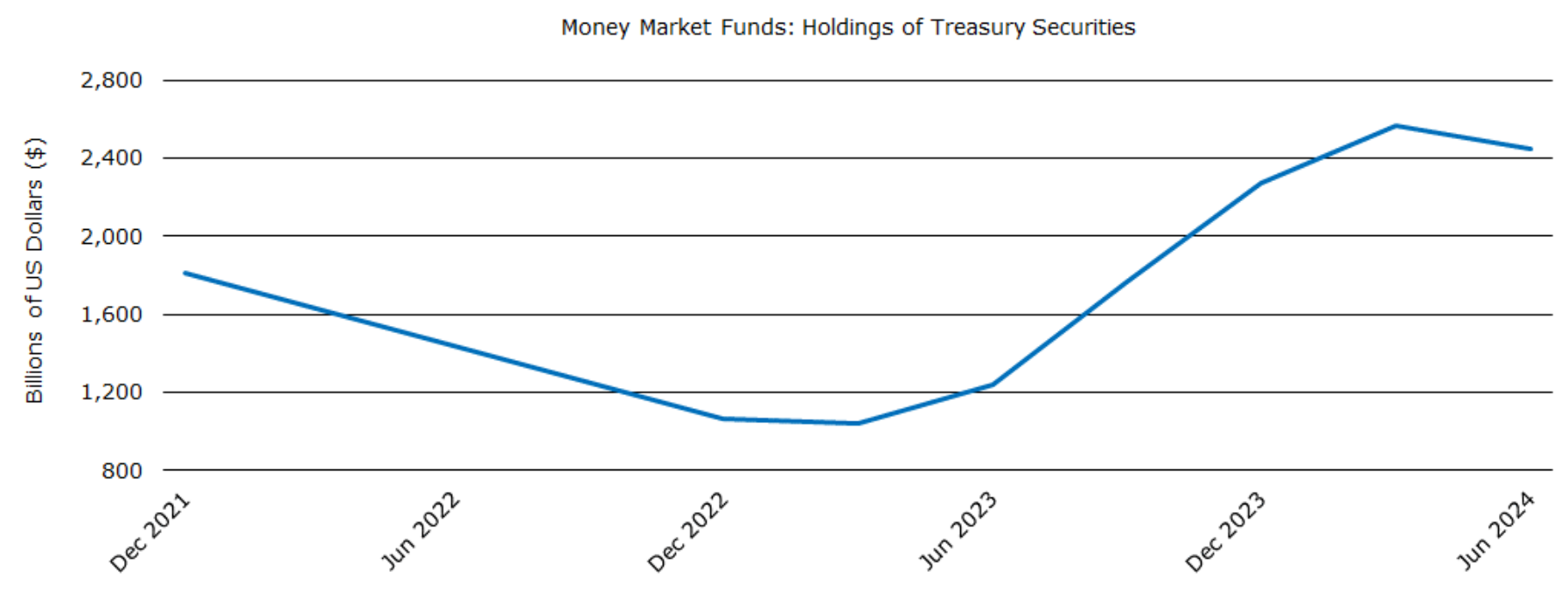

Demand for Treasuries: Foreign Holdings, US Households, Money Markets, and Repo Market

We now turn our attention to the sources of demand for US Treasuries since the beginning of 2022. Foreign Holdings of Treasuries: Since early 2022, foreign holdings of US Treasuries have increased from $7.74 trillion to $8.5 trillion. The modest increase indicates a reduced appetite among foreign investors for acquiring US Treasuries.

US Households: According to Federal Reserve data, household holdings of Treasury securities have risen significantly from $498 billion at the end of 2021 to $2.75 trillion in Q2 2024. This growth has absorbed a substantial portion of the increase in Treasury supply.

Money Market Funds: In contrast, money market funds have seen a modest increase in Treasury holdings, rising from $1.8 trillion at the end of 2021 to $2.45 trillion in Q2 2024, which is modest increase.

Repo Market: Technically, the repo market does not function as an “investor” or “holder” of Treasury securities; rather, it serves as a financing mechanism for holders of these securities, allowing them to pledge and borrow against their holdings. In this context, it acts as a proxy for “leveraged” players in the Treasury market , including hedge funds (such as macro and multi-strategy funds) and other participants using leverage – sometimes up to 50x – to finance their Treasury holdings.

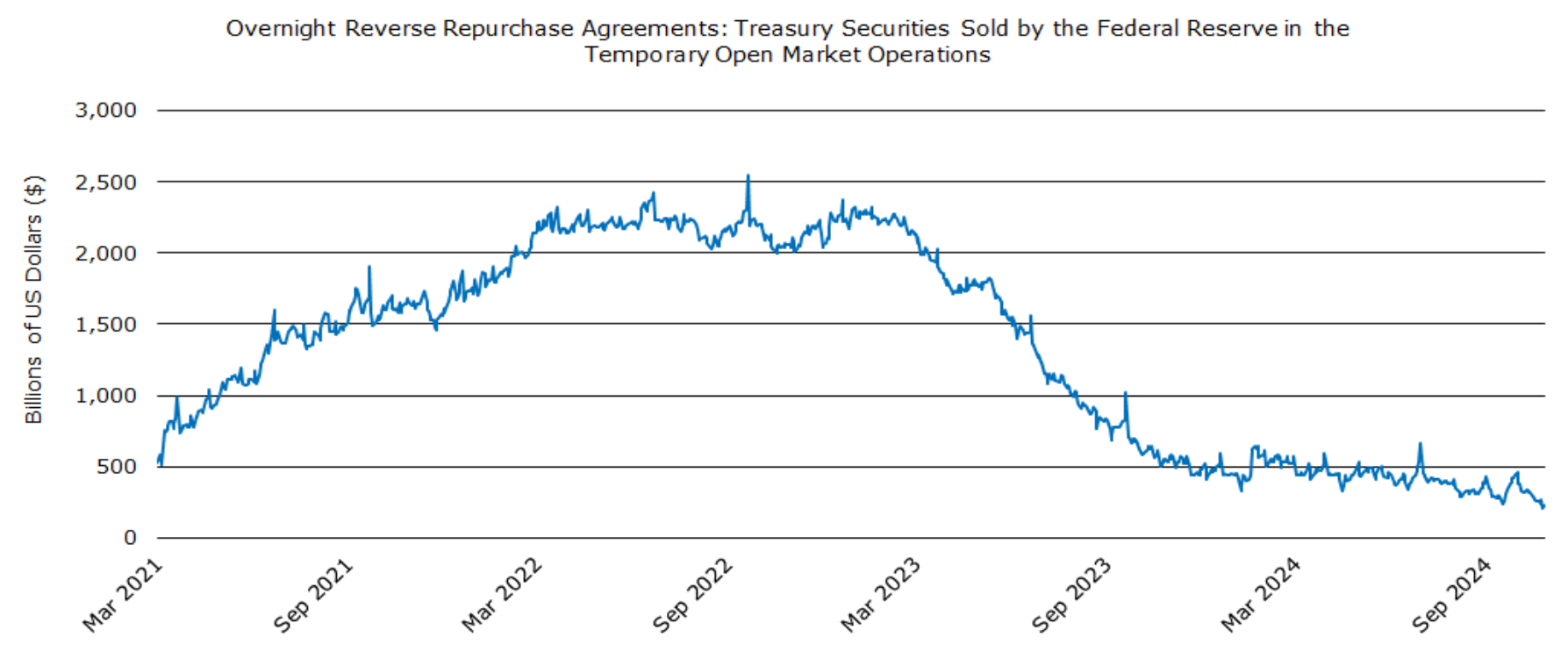

The Office of Financial Research (part of the US Treasury Department) has published . data on repo transactions According to their data, repo volumes have increased from $3.88 trillion at the end of 2021 to $4.88 trillion at the end of Q3 2024, reflecting a growth of $1 trillion, or over 25%, in the past 30 months. However, this is not the complete picture. Another important data point is the Federal Reserve’s influence on repo market volumes. The Fed has been an active participant in the repo market over the past three years. The accompanying chart illustrates the volume of the reverse repo market since March 2021, showing the volume of reverse repos executed by the Fed. In these operations, investors provide repo financing to the Fed, which in turn conducts reverse repos on Treasuries, offering a return to investors. During periods of quantitative easing, when market liquidity was abundant, money market funds and other players utilized excess liquidity to provide funding to the Fed, which the Fed used to finance its Treasury and other securities holdings.

At its peak in 2022, the size of the Fed’s r everse repo program reached $2.4 trillion, but it has since declined significantly to $202 billion as of October 24 th . Essentially, the reduction in the Fed ’s reverse repo facility, which diverts repo financing from other uses, effectively provides additional liquidity in the repo market. If we define " true open market repo " as the difference between total repo volumes and the repo utilization by the Fed, this figure has increased from $2.18 trillion at the beginning of 2022 ($3.88 trillion total repo volume minus $1.7 trillion Fed reverse repo volume) to $4.68 trillion in October 2024. This indicates that a substantial amount of Treasuries – likely more than $2.5 trillion – has been absorbed by market participants utilizing the repo market.

US Households and Leveraged Buyers: Key Sources of Incremental Demand for US Treasuries

Our analysis reveals that of the approximately $5.7 trillion increase in US debt since the end of 2022, $4.7 trillion has been absorbed by households and leveraged buyers.

However, the full picture is more complex. During this period, the Federal Reserve has sold approximately $1.3 trillion of Treasuries. Consequently, between Fed sales and Treasury issuance, around $7 trillion of Treasuries has entered the open market, with $4.7 trillion – representing 67% – absorbed by households and leveraged buyers. Foreign purchasers and money market funds have also contributed significantly to this demand. The significant role of household and repo purchasers has important implications for pricing in the Treasury market.

Demand for Positive Real Yields from Household Purchasers May Lead to Portfolio Adjustments

Household purchasers, who typically hold Treasuries in their brokerage accounts, are likely to demand positive real yields. Therefore, it is crucial for the Federal Reserve to maintain a disciplined approach to controlling inflation. If the Fed loses credibility in its fight against inflation, these household purchasers may require even higher yields to consider adding Treasuries to their portfolios – or even to retain their current holdings. Additionally, household purchasers may need to adjust their portfolios to accommodate more Treasuries. This could lead them to become net sellers of other asset classes, such as equities, corporate bonds, and real estate. The net effect would likely result in higher Treasuries yields and lower valuations for other asset classes.

Repo Purchasers May Encounter Limited Capacity and Increased Volatility

Conversely, repo purchasers may not be particularly sensitive to real yields in the short term. Instead, they may base their decisions on the technical pricing of Treasuries or the potential to earn positive carry from their holdings (i.e., the difference between financing costs and Treasury Yields, as well as the steepness of the curve). However, we believe the growth of the repo market may face significant challenges maintaining its current pace. While the market has expanded by 25% over the past 30 months, further growth may encounter strong headwinds. For instance, bank balance sheets are not increasing at the same rate, and anecdotal evidence suggests that banks are beginning to experience constraints on their repo capacity. Banks rely on deposits or other funding sources to support their repo operations, and, in the absence of additional repo facilities from the Fed, we are skeptical about the repo market ’s ability to continue growing at this rate. Moreover, the repo market may come under increased scrutiny, as it represents a highly leveraged form of financing that carries potential systemic risks. As Congress raises the debt ceiling in the coming months and the Treasury Department issues additional Treasury securities, this market is worth monitoring.

Market Views

Given our outlook that long-term yields are likely to rise, we are exercising caution in our risk-taking and transaction structuring. We believe that focusing on downside protection remains essential.

Disclosures

The information contained in this document is for informational purposes only and should not be considered investment advice. This document does not constitute an offer to sell, a solicitation of an offer to buy, or a recommendation for any security or investment strategy.

Past performance is not indicative of future results. All investments carry risk, including the possible loss of principal. The views expressed herein are those of the author as of the date of publication and are subject to change without notice.

Forward-looking statements are based on current expectations and assumptions, which are subject to risks and uncertainties. Actual results may differ materially from those anticipated.

Monachil Capital Partners LP is a private investment firm. Investment opportunities described herein may be available only to qualified purchasers as defined under the Investment Company Act of 1940.