Introduction and Overview

Welcome to our September 2024 monthly report. As is our practice in these commentaries, we aim to highlight topical matters and assess their potential impact on financial markets. After discussing the housing market in our previous letter, we return to discuss recent developments in the macroeconomic outlook. Most notably, we believe the Fed made a mistake by cutting the interest rates by 50 basis points at their September meeting. Although short-term inflation has eased slightly in recent months, the August CPI report indicates persistent inflationary pressures and the need for significant resistance to reach the 2% target. In this report, we will also continue to cover signs of stress in the US treasury market. While, overall, the yield and price of the treasury market are behaving normally, there are some nuanced signs of stress in the repo market with treasury yields moving wider than the repo rates. This brings us to the challenges imposed by the increasing supply of US treasuries and the United States’ worsening fiscal picture, which makes a soft landing increasingly unlikely.

U.S. Soft Landing Remains Unlikely, Fiscal Pressures to Drive Instability

Recent lower inflation prints have renewed market participants’ confidence in the possibility of a soft landing. However, we continue to view these expectations as premature and too optimistic, especially considering the deteriorating fiscal outlook of the U.S. federal government. A true soft landing – or any type of sustained equilibrium – requires not only steady growth and low inflation but also a healthy fiscal environment. Having the first two without the third is unstable at best. History offers numerous examples, such as Greece and the UK in the early 2010s, where growth and low inflation were undermined by fiscal instability, ultimately leading to economic downturns. Of course, the way such imbalances play out is pathand policy-dependent, and the mere existence of such imbalances does not necessarily represent calamity in the financial markets. These adjustments could be achieved by higher taxes, reduced government spending, prolonged increases in inflation, or a mix of these factors. How these dynamics ultimately unfold will eventually depend on the political and policy decisions made by the government. Given this uncertainty, we see the current combination of low inflation and steady economic growth as “transitory” at best . However, we believe the process through which these adjustments take shape will create opportunities for investors and market participants.

Increased Strains in the Treasury Repo Markets

As mentioned earlier, one area where we are observing increased market pressure and stress is the treasury repo markets. On the surface, both the treasury markets and the repo markets appear to be functioning normally. However, a closer examination of

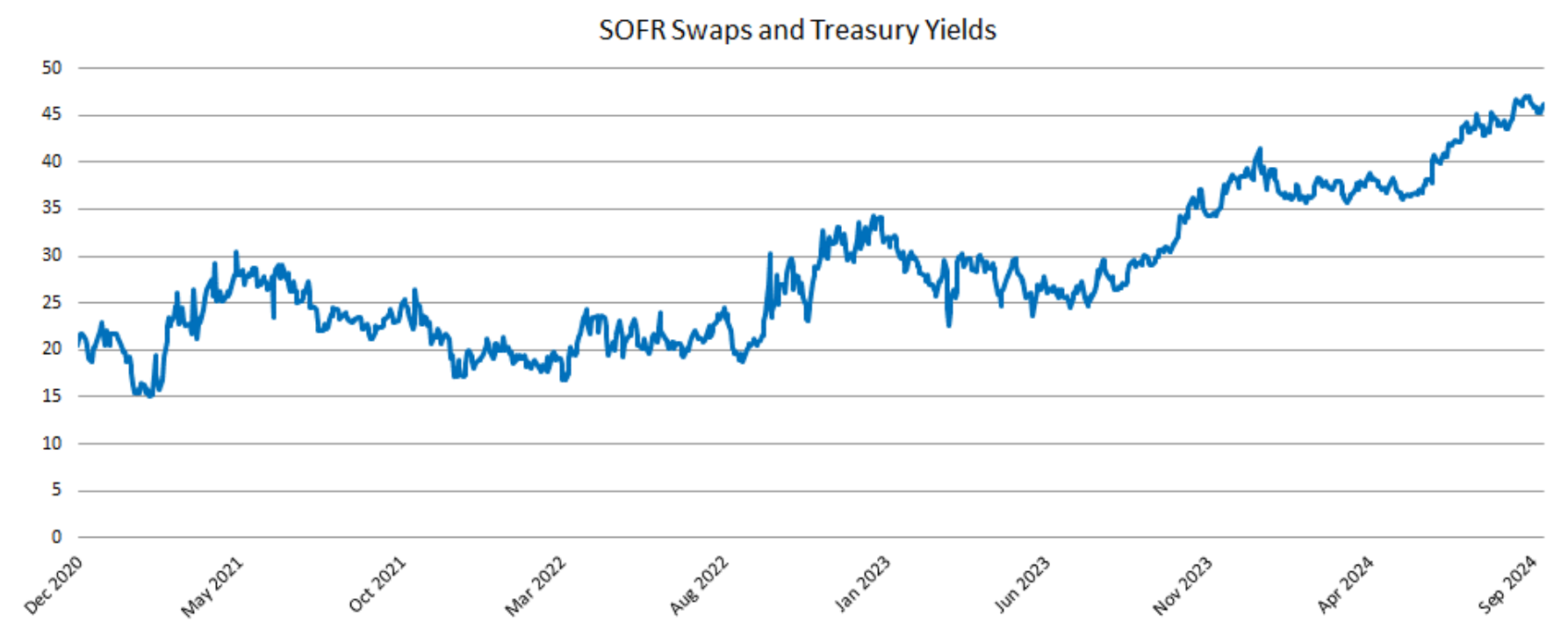

the spread between repo rates and treasury yields over the past five years reveal underlying issues. Essentially, spreads have widened from around 20 basis points to 45 basis points, with roughly 10 basis points of that increase occurring in the last four months (see Figure 1).

The chart above illustrates the difference between SOFR swaps and treasury yields, where a positive value indicates treasury yields are exceeding repo rates. This shift suggests that investors are demanding higher yields relative to the cost of treasury repo, signaling a change in the behavior of treasury investors. The marginal buyers of treasuries are increasingly relying on the repo market to finance their treasury holdings. As the supply of treasuries grows, these investors require a larger spread to continue purchasing more treasuries. This dynamic contrasts sharply with the situation a decade ago, when the buyers of treasuries were primarily outright purchasers, and yields traded more tightly relative to long-term swaps.

Backdoor Quantitative Easing: The Fed is Indirectly Financing the Federal Government Through the Repo Market

While the official stance is that the Fed has been tightening the monetary policy through higher interest rates, the Federal Reserve has also employed various balance sheet measures to support the treasury market, effectively implementing different forms of quantitative easing. One such mechanism is the Federal Reserve’s support of the repo market. Primary dealers and banks with access to the Fed’s repo facilities act as intermediaries between holders of treasuries and repos’ “end users” , so to speak, a group that includes hedge funds and other market participants. These end users can then monetize the spread between treasury yields and repo rates. With the high amounts of leverage available in the repo market, they are able to generate significant profits from this differential.

However, this mechanism poses several risks to the broader economy:

- Increased Money Supply

With the Federal Reserve increasingly backing the repo market through its balance sheet, the expanding repo market is contributing to a rise in the overall money supply.

- Increased Systematic Risk

Although the repo markets have a strong track record, an increased reliance on them to keep the treasury market functioning introduces systematic risk. In adverse market conditions, this could potentially lead to forced liquidations of treasury holdings. A similar disruption was witnessed during the UK Gilts crisis in 2022, when margin posting requirements for rate hedges triggered forced selling in the Gilts market, destabilizing government securities.

- Back Door Financing of the Federal Government by the Central Bank

This also serves as a less transparent method for financing federal government deficit spending via the central bank, using banks and hedge funds as intermediaries.

What we will keep an eye on:

We will continue to closely monitor this space, particularly for further widening of the spreads between treasury yields and SOFR swaps.

Deficits, as the Primary Driver of Treasury Supply, are Worsening

In September, the Congressional Budget Office (CBO) released its monthly budget review for the first 11 months of fiscal year 2024, painting a grim picture. The federal budget deficit reached $1.9 trillion over this period, indicating that deficits will exceed $2 trillion for the second consecutive year . While the “official” deficit for 2023 was reported at $1.7 trillion, this figure was artificially lowered by about $300 billion due to a budget gimmick related to student loans. This adjustment does not reflect the true impact of the Supreme Court ruling and subsequent executive actions, which will not be felt for years. We believe federal deficits will remain persistently high, around 6-8% of GDP, and will increasingly act as a drag on economic growth. Maintaining the deficit at this level relative to GDP will require higher debt service costs, straining government finances. Currently, approximately $1 trillion, or half of the annual deficit, represents the cost of servicing debt. This growing debt load will continue to fuel an expanding supply of treasury issuance, which, in our view, will eventually overwhelm the capacity of the repo market to absorb it in the medium term.

Fed Makes a Mistake by Doing a Jumbo Cut of 50 bps While Inflation is Still Above Target

A notable event in recent weeks has been the Federal Reserve ’s substantial rate cut. We believe the Fed made an error in executing such a large cut while inflation remains

above target and financial conditions are relatively loose. The Fed could have just as easily chosen to accelerate the pace of rate cuts later, should the data warrant it, but instead they acted with abandon. Additionally, the focus on the so-called “employment mandate " often seems like a jus tification for keeping rates low, regardless of broader economic conditions. The risk the Fed faces with its lenient policy is that it may leave itself with fewer tools to address future crises. With equity valuations and corporate earnings at all-time highs, this rate cut seems unnecessary, especially in light of the stronger-thanexpected August CPI reading. We believe the market is underestimating the significance of upcoming CPI data, which could force the Fed’s hand. For now, the Fed is being aided by falling commodity prices, which will temporarily ease inflationary pressures. However, given the scale of federal deficits and the Fed’s ongoing monetization of federal debt, inflationary pressures are likely to remain elevated over the medium term.

More Opportunities on the Short Side

While the market remains euphoric, we see this as an opportunity to enhance our protective positioning. Some of our strategies were put to the test on August 5th, when a sharp rally in the Japanese Yen destabilized equity markets. During that brief period of volatility, we were satisfied with the performance of our hedges, reaffirming the importance of maintaining a defensive stance in the current environment.

Disclosures

The information contained in this document is for informational purposes only and should not be considered investment advice. This document does not constitute an offer to sell, a solicitation of an offer to buy, or a recommendation for any security or investment strategy.

Past performance is not indicative of future results. All investments carry risk, including the possible loss of principal. The views expressed herein are those of the author as of the date of publication and are subject to change without notice.

Forward-looking statements are based on current expectations and assumptions, which are subject to risks and uncertainties. Actual results may differ materially from those anticipated.

Monachil Capital Partners LP is a private investment firm. Investment opportunities described herein may be available only to qualified purchasers as defined under the Investment Company Act of 1940.