Introduction and Overview

Welcome to our July 2024 monthly report. As is our practice in these commentaries, we aim to highlight topical matters and assess their potential impact on financial markets. In this report, we discuss the recent rally in credit spreads and the ongoing risks of economic imbalances. Specifically, as previously observed in our March 8, 2024 Commentary, the recent moderation in the housing component of the CPI does not align with the lofty valuations we are seeing in the housing market. While we do not have a definitive view on whether housing (or other real estate) valuations should decrease or rents should rise, we believe that a market adjustment in one or both aspects of housing is necessary. Over the past few weeks, there has been commentary, including from the Fed Chairman, suggesting that interest rate cuts could help reduce housing inflation. We believe that the Chairman’s reasoning is flawed (in this instance, at least) as it conflates correlation with causation. We will return to this topic further later in this report. We wonder whether the Fed’s soft touch on inflation and the easing of financial conditions might actually – and unintentionally - lead to the creation of asset bubbles. As such, we question if the expected rate cut in September, which currently seems like a foregone conclusion, is a wise move.

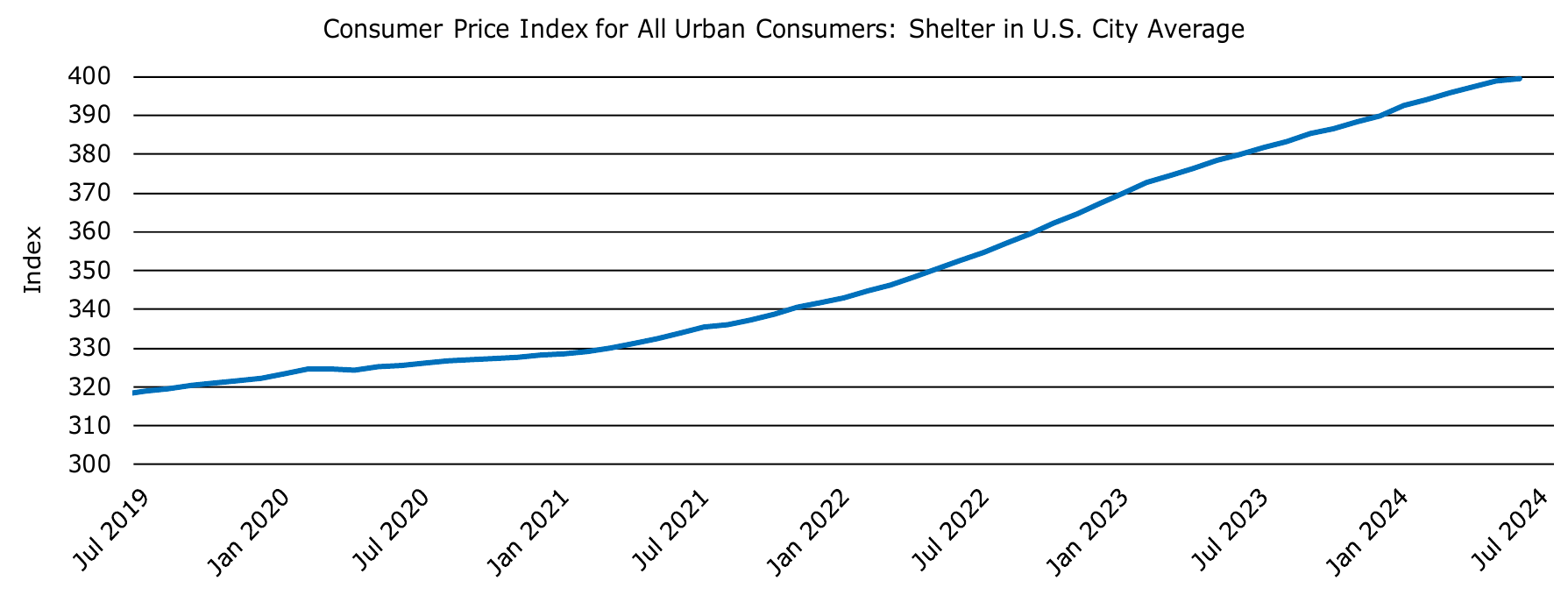

Inflation In June Shows Easing, Including Material Decline in Shelter

The June 2024 CPI report showed a decline of 0.1% on a seasonally adjusted basis, while the 12-month CPI showed an increase of 3%. For context, the last time this figure was below 3.0% was in March 2021. Shelter inflation, which includes both Rent of Primary Residences and Owners’ Equivalent Rent of Residences, rose by 0.2% month over month and 5.2% over the past 12 months. We are somewhat skeptical of this reading as it indicates that rents continue to lag significantly behind housing valuations. We believe that if real estate valuations and rents were to converge, it would require substantial adjustments in one or both, which would also impact the credit markets. Additionally, we note that Energy Inflation is at 1% year-over-year, which we find somewhat puzzling. While headline energy prices may not be increasing, there are hidden costs in the form of renewable energy subsidies which are not reported as inflation. These costs are reflected in the deficit and could eventually impact the markets through either higher government borrowing or an increase in central bank financing of deficits.

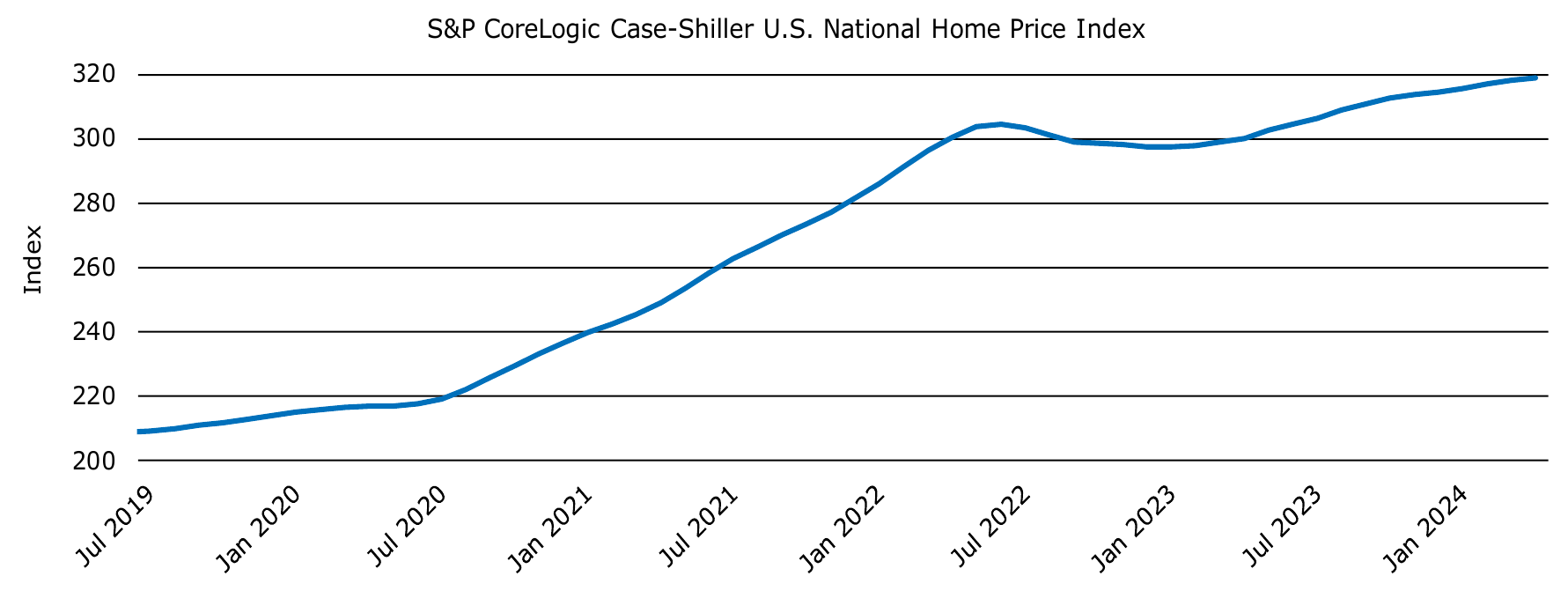

Lower Shelter Inflation is inconsistent with Home Price Growth

While both Shelter Inflation and Home Price Growth have shown signs of moderation, there remains an apparent imbalance between the two. Over the past 5 years, home prices have increased by 50%, while rents (including third-party rents and Owner s’ Equivalent Rents used in CPI calculations) have risen by only approximately 30%.

All else being equal, this divergence between prices and rents is unsustainable and needs to be resolved. Additionally, with interest rates sitting higher than they were 5 years ago, equilibrium home prices should, in theory, be lower. This imbalance in the housing market is worth monitoring as it raises questions about whether rents will need to increase or home prices will need to decrease to restore equilibrium. Furthermore, there are other idiosyncratic factors driving home demand, including certain tax advantages that have made owning rental property more attractive following the Tax Cuts and Jobs Act of 2017. Notably, some of these tax advantages include bonus depreciation, qualified business income, and expanded Section 179 expensing.

Marginal Buyers and Sellers of Housing

Like any other market, the price of housing is generally set by marginal buyers and sellers of houses. While the incentives we mentioned above might increase demand for entities and individuals to become landlords, the impact of this demand on prices is likely to be

somewhat transitory (there, we said it!). Once this demand is met, housing prices will be dependent on the equilibrium between production costs (land, material, labor) and value of ownership. In other words, the short-term marginal supply of housing is driven by “existing homes , " while the medium-to-long-term marginal supply is determined by new construction. There could be a temporary demand shock from entities and individuals purchasing investment properties (and needing to find tenants). However, once this demand is satisfied, long-term equilibrium pricing will be determined by the fundamentals of production costs and the utility of ownership (i.e., the value of owning a house). Thus, while post-2017 tax incentives and Covid-era dynamics may create new marginal buyers in the housing market, including those from rental property operators (both long-term and short-term), the marginal buyer, in the long run, will likely return to being a consumer purchasing a home for its utility and shelter. In recent months, we have observed some of the dynamics mentioned in this section. Data from Zillow Research indicates that, in some markets, new homes are selling at a discount per square foot compared to existing homes. As time goes on, we believe this trend will help moderate housing prices.

Price and Valuation of Housing and Inflation Dynamics

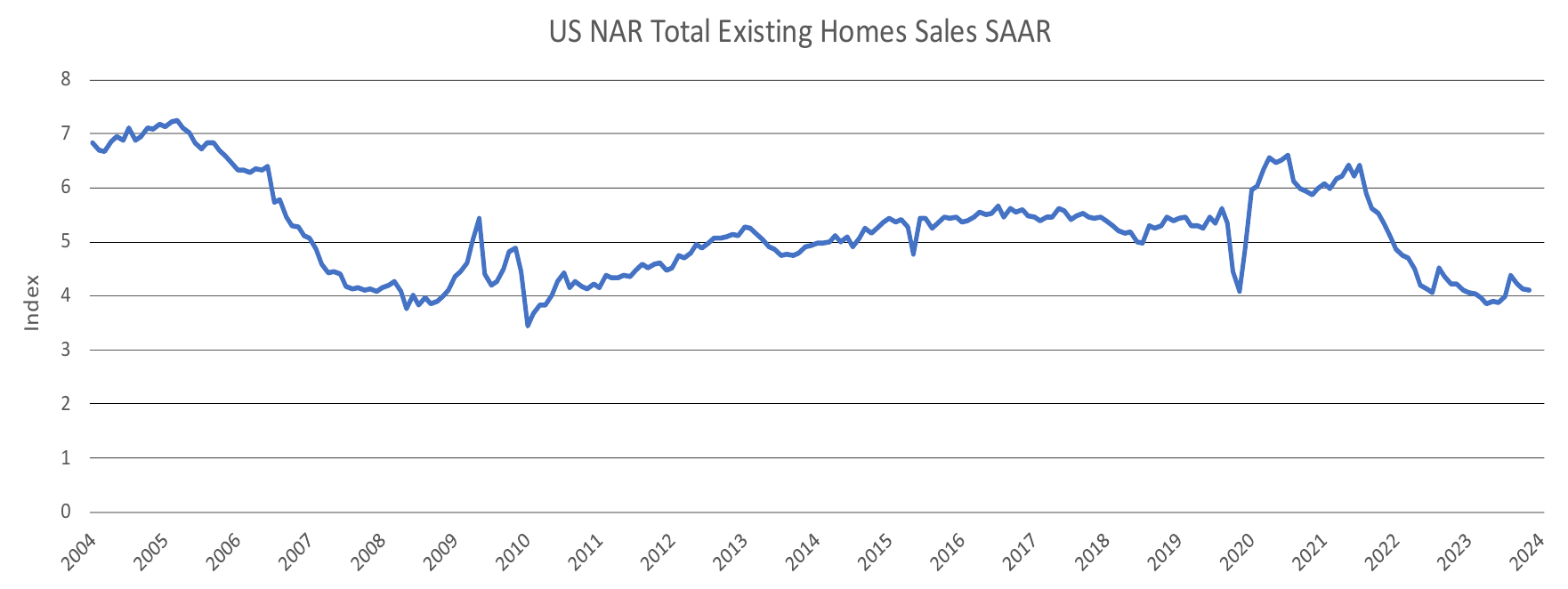

Rents are a reliable metric for measuring the utility value of shelter and homeownership. Over the past decade, increased allocation to Single-Family Rentals (SFRs) as an asset class has provided more data to measure the ongoing value of shelter expressed in monthly rents. If rents were to increase only at the rate of inflation, and if inflation were to hit 2%, then it is highly likely that home prices would begin to decline, albeit gradually. The discounted cashflow value of owning a home and being a landlord is determined primarily by rents and interest rates (excluding other factors such as expenses and taxes for simplicity). Conversely, if inflation is brought under control, it is likely that some input costs of housing might not only stop appreciating, but could potentially decline like we have seen in lumber prices. In our view, if the main goal is to reduce home prices effectively, focusing on policies that lower input costs, such as those for energy and materials, might be more impactful than offering other types of incentives. Current rent levels compared to ownership costs suggest that renting is economically more advantageous. We are seeing this dynamic reflected in home sales statistics. In June, existing home sales declined by 5.4% from the previous year to a seasonally adjusted rate of 3.89 million, while sales prices rose by 4.1% from a year earlier. This sharp decline in volume aligns with figures observed in 2010, although inventory was higher back then. Similarly, new home sales are also declining, though at a slower rate. A correction in housing prices, as long as it remains orderly, will have a limited impact on the credit markets, and the impact there will be through losses in bank books which could restrict the supply of other forms of credit. The more credit-intensive parts of the real estate market (which include office and multifamily properties) are already going through their valuation adjustments and have started impacting bank balance sheets.

That said, we continue to maintain our view that public credit markets do not currently offer compelling values and instead are more focused on private and bilateral transactions.

This does not imply that there is no housing shortage or that the housing market is on the brink of collapse. Rather, it indicates that the dynamics that were driving up home prices during the Covid era are no longer as influential. However, if rental demand remains strong, we expect housing inflation, as reflected in rental prices, to persist.

Cutting Interest Rates Would Not Drive Down Housing Valuations

We have observed increasing commentary from both politicians and some economic forecasters suggesting that reducing interest rates is necessary for lower housing costs. However, we believe many of these arguments are misguided and incorrect. First, there is often confusion between causality and correlation. While it is true that periods of low inflation generally coincide with both low housing inflation and low interest rates, lowering interest rates does not necessarily cause housing prices to decrease and, in fact, high interest rates do not necessarily lead to higher housing prices. Actually, having interest rates that are lower than the rate of inflation would create more demand for hard assets, including housing, which will drive prices higher. This is one of the mechanisms by which lower interest rates can expand the money supply. Another more nuanced argument suggests that higher interest rates are making many construction projects uneconomical, thereby reducing the housing supply. We find this argument flawed as well since it assumes that high interest rates, when used to discount cash flows and assess project valuations, result in lower valuations, making some projects non-economical. Lowering interest rates would likely push housing prices higher, doing little to address affordability issues and primarily making financing cheaper without solving the underlying problem. So, if the goal of cutting interest rates is to make construction projects economically viable by pushing up housing prices (and real estate prices), we see some likelihood that this would be counterproductive and inflationary.

A further argument in favor of cutting interest rates to lower housing prices is that interest expenses of construction loans drive up construction costs. However, we find this argument unconvincing. Construction loans, which carry high spreads, are only partially affected by changes in risk-free rates and Fed policy rates. Additionally, construction loans typically have short durations (usually less than 3 years), in contrast to mortgages or other financial products used for purchasing real estate. As a result, any reduction in construction costs is likely to be outweighed by the increase in purchasing prices that buyers are willing to pay when interest rates are lowered.

Impact on Credit Markets

A correction in housing prices, as long as it remains orderly, will have a limited impact on the credit markets. Most of the impact will come from losses on bank balance sheets, which could restrict the supply of other forms of credit. The more credit-intensive sectors of the real estate market, such as office and multifamily properties, are already undergoing valuation adjustments and have begun affecting bank balance sheets. That said, we continue to maintain our view that public credit markets do not currently offer compelling value and are instead directing focus to private and bilateral transactions.

Disclosures

The information contained in this document is for informational purposes only and should not be considered investment advice. This document does not constitute an offer to sell, a solicitation of an offer to buy, or a recommendation for any security or investment strategy.

Past performance is not indicative of future results. All investments carry risk, including the possible loss of principal. The views expressed herein are those of the author as of the date of publication and are subject to change without notice.

Forward-looking statements are based on current expectations and assumptions, which are subject to risks and uncertainties. Actual results may differ materially from those anticipated.

Monachil Capital Partners LP is a private investment firm. Investment opportunities described herein may be available only to qualified purchasers as defined under the Investment Company Act of 1940.