MARKET AND ECONOMIC INSIGHTS

April 30, 2024

Introduction and Overview

Welcome to our April 2024 monthly report. As is our practice in these commentaries, we aim to highlight topical matters and assess their potential impact on financial markets. Regular readers of our letters will know that we remained steadfastly contrarian as the Fed and many market commentators began touting an imminent defeat of inflation. So far this month, economic data vindicates our view in revealing inflationary pressures persisting into March. We have consistently warned that the pattern of large deficit spending is, in and of itself, inflationary and, in our prior letter, we opined that the Federal Reserve has been adding fuel to the inflationary fire by encouraging the formation of asset price bubbles with loose and overly accommodative interest rate decisions. In this report, we delve deeper into the Fed’s failure to control inflation, but first we will take a brief foray into the details of bank earnings to see what they reveal about the dynamics of credit markets. In particular, we have detected signs that indicate that the long-lasting higher interest rate environment may impact banks differently this time versus what history might have suggested, and that there may even be harbingers lurking of a kind of structural shift that bears close attention.

Net Interest Income Growth at Large Banks Disappoints, but This Was Inevitable

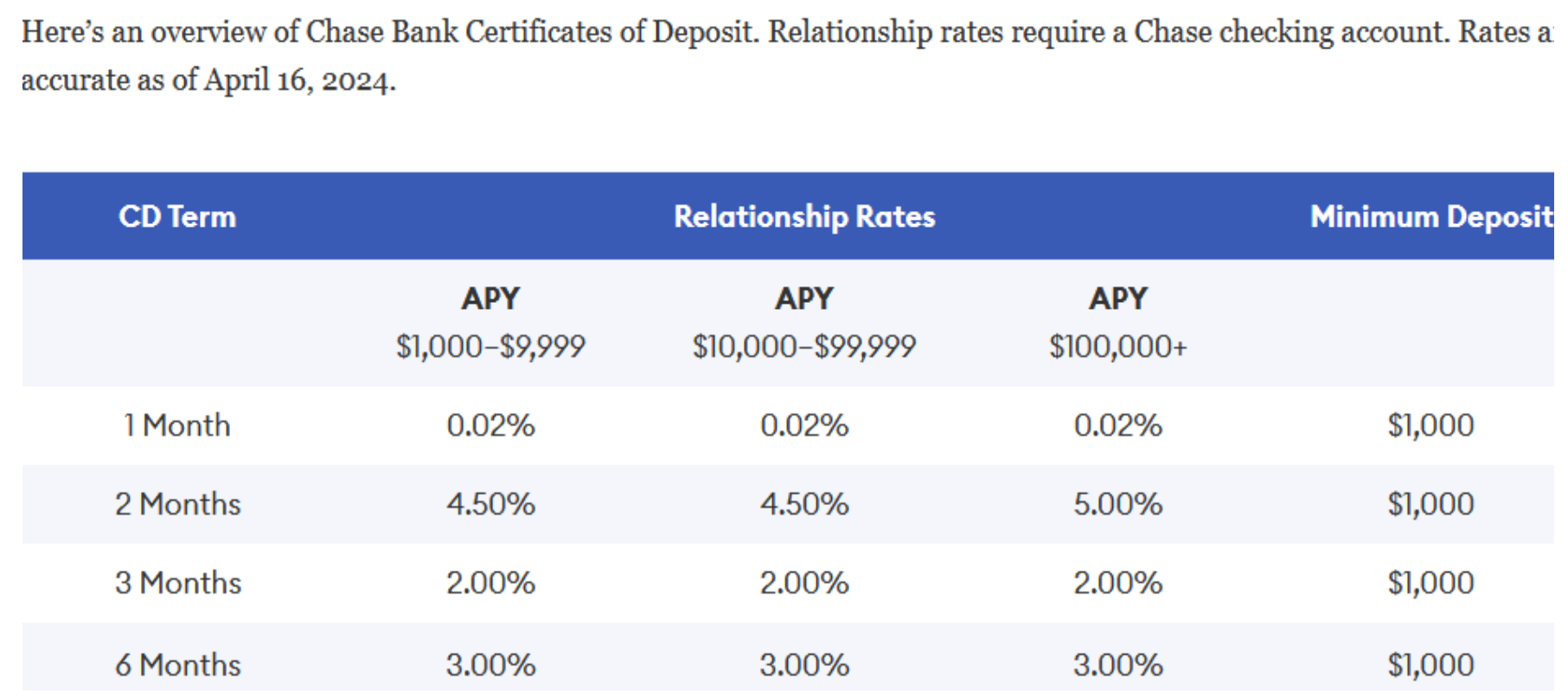

We typically refrain from commenting on bank earnings, but we believe that this quarter’s market reaction to JPM’s earnings can provide valuable insight. JPM’s net interest income was $23.20 billion, falling short of the estimated $23.22 billion. The net yield on interest-earning assets came in at 2.71%, also missing the estimated 2.75%. This was followed by a 6% decline in share price (although it should be noted that JPM’s earnings release coincided with a down market day). Many commentators attribute the stock price weakness to the “NIM miss.” We believe that the markets reacting so severely to a relatively small deviation in earnings is indicative of irrational expectations. Let’s face it, a 0.04% difference in NIM is not statistically significant. We wonder if the market reaction had less to do with a near miss than the cold shower effect of realizing the party may be over. After all, the absolute amount of net interest income has ballooned over the past few years. In 2020, the NIM was $61.53 billion, which grew It is not rational for the markets to expect such growth in NIM over a long period. To achieve this, JPM would need either to continue to expand its balance sheet at such a high rate or to earn a much higher net yield on its interest-earning assets. The following chart is what our search of online CD rates at JP Morgan has produced.

Navigating this challenge is proving to be daunting for JPM, as it would for any other bank. Presently, JPM offers close to 0% on its standard Chase Savings account and 3% on its Chase Standard CD. However, as T-Bills persist above 5% for longer durations, convincing customers to retain their cash in products with significantly lower yields becomes increasingly challenging. Even within the same depository, the composition of deposits is shifting as customers begin to transfer their balances from non-interest-bearing options (such as regular deposit accounts) to CDs that offer higher rates. In their most recent quarterly earnings, both Wells Fargo and JP Morgan cited increased pressure to allocate more funds for deposits as one of the drivers for weaker Net Interest Incomes (NIIs).

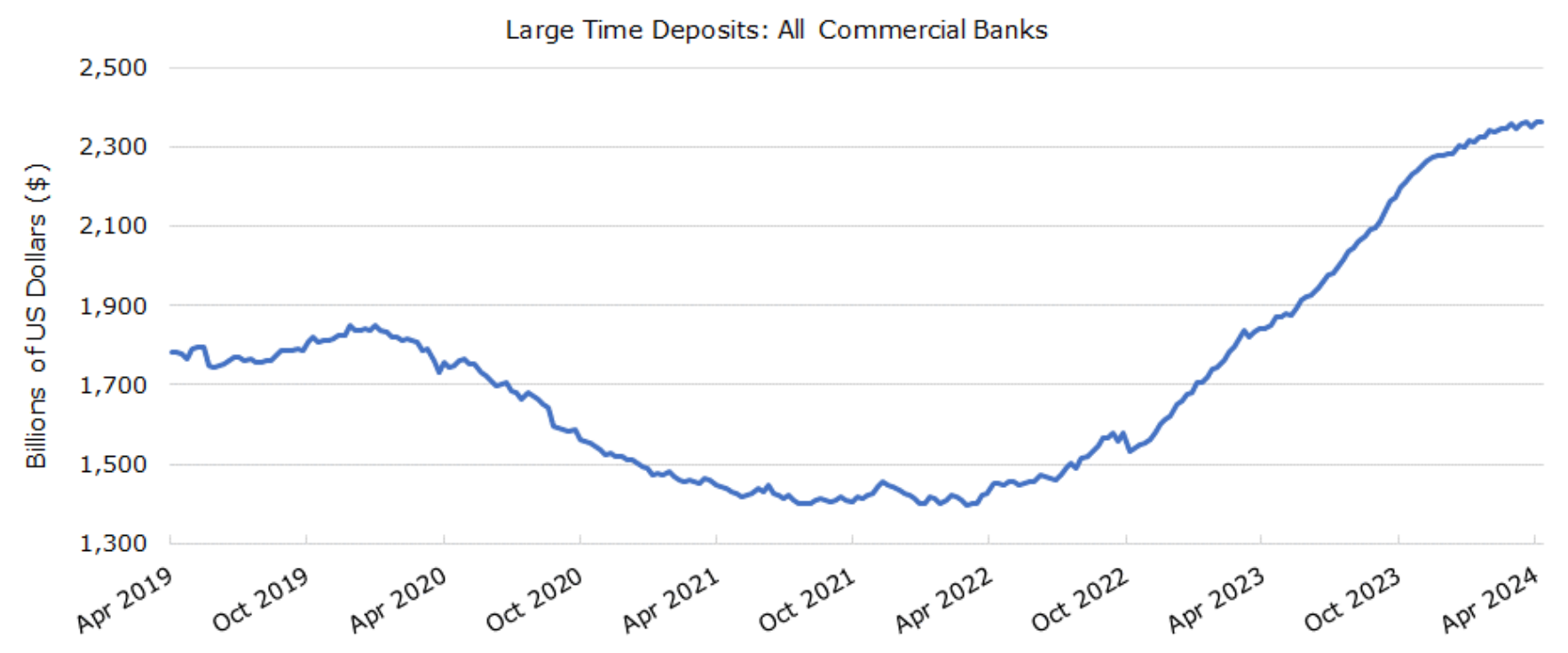

The chart above illustrates the significant increase in large deposit balances over the past years. Compared to the levels seen in 2021-2022 at the height of zero interest rates, high-interest-paying balances have nearly doubled. Among other factors, the interest that high-interest deposits can earn has increased dramatically. In our view, this has the potential to create some downside risk for banks in general and to make credit extension by the banks a less lucrative business. On one hand, the large volume issuance of T-Bills by the US Department of Treasury is creating competition for bank deposits. At the same time, the higher rates on T-Bills will gradually force the banks to pay more and more on the deposits to attract savers. Therefore, the dynamics for bank earnings during this hiking cycle could end up being very different.

Inflation Continues to Move Higher

The Consumer Price Index for All Urban Consumers (CPI-U) increased by 0.4% in March on a seasonally adjusted basis. Over the past 12 months, the " all items index " has risen by 3.5%, representing a larger increase compared to the 3.2% rise for the 12 months ending in February. We have been warning about the possibility of inflation being more persistent than what the Fed is assuming, or at least what its public statements have been suggesting they believe. The increase in CPI has been primarily driven by a 5.7% increase in shelter costs, which accounts for 36% of the CPI index. Another notable item is motor vehicle insurance, which has increased by 22.2% year-over-year. Energy prices have seen a 2.1% increase year-over-year, but since March energy prices have moved even higher. We anticipate that the combination of higher energy and commodity prices, as well as increased shelter costs, will sustain higher levels of inflation.

Fed’s Monetary Policy is Not Adequately Restrictive, Indicating that the Neutral Rate of Interest Rates is Higher than the Fed Assumes

The acceleration in inflation is a worrisome trend as it indicates that the current monetary policy is not adequately restrictive given the totality of the economic conditions. In light of this, the comments made by Fed officials since November 2023 seem to be particularly misguided . For reasons unbeknownst to us, Fed officials, including chairman Powell and governor Waller, decided that it was a good idea to pump the markets by discussing inflation in a negative light and signaling that they are merely searching for any possible excuse to lower rates. Thanks to their rhetoric and that of other Fed officials, inflation appears to be reaccelerating with the wealth effect of higher equity prices dependably is sustaining demand. As inflation continues to rise, the benefit of past rate hikes is beginning to diminish, indicating that the current interest rates may not be as restrictive as the Fed has been assuming.

Retail Sales Have a Strong Showing, Further Removing Urgency for Rate Cuts

In an indication that current inflationary pressures are poised to persist, monthly retail sales for the month of March reached $709.6 billion, representing a +0.7% increase month over month. According to the U.S. Census Bureau, these numbers reflect a 3.6% inflation (albeit marginally, as CPI stood at 3.5%), and signs of monthly acceleration suggest heightened inflationary pressures within the economy. This serves as additional evidence that the current level of interest rates is not sufficiently restrictive to control inflation.

As The Fed Keeps Delaying Tackling Inflation, Higher Interest Rates are Looking Likely to Last Longer

The jawboning by Federal Reserve officials mentioned above has not been without cost. As markets and consumers begin to question the Fed’s credibility in combating inflation; and inflation expectations start to rise, higher interest rates are appearing increasingly necessary. Indeed by hastily attempting to buoy equity markets, the Fed has merely cornered itself, where sooner or later it will need to address the prospect of additional rate hikes toward (possibly) higher terminal rates. In an alternate scenario, where the Fed had maintained a disciplined approach to fighting inflation, higher interest rates might not have become necessary. Consequently, in our opinion, the Fed’s approach over the past few months is starting to resemble another policy mistake that we have to attribute to their underappreciation of the most prominent driver of inflation: government spending, and the everexpanding enormity of Federal deficits.

Deficit Spending by Federal Government is Expanding with Hardly Any End in Sight

The CBO released its monthly budget review for March 2024 on April 8th, 2024. The federal budget deficit amounted to $1.1 trillion in the first half of fiscal year 2024 (October 2023-March 2024), consistent with the deficit recorded during the same period last fiscal year. The CBO is inaccurately projecting the deficit for the fiscal year to be approximately $1.5 trillion. We believe their numbers are severely misguided and will need revision. One reason for this assertion is that the cost of debt service is likely to continue rising this year. Additionally, last year’s official deficit came was $1.7 trillion, but that included a roughly $300 billion accounting gimmick resulting from the Supreme C ourt’s rejection of the administration’s proposal for student loan forgiveness, which reduced the deficit. That benefit was one-time, and if it applies to the current fiscal year, it might shift in the opposite direction, with the administration’s student loan proposals potentially contributing to the deficit. April is a pivotal month for the fiscal outlook as it sees the highest amount of tax receipts. As of mid-April, the outstanding balance in the Treasury General Account (TGA) indicates robust tax receipts. However, we anticipate that for the remainder of the year, these receipts will be outweighed by expenditures, putting the deficit on a trajectory to surpass $2 trillion.

Money on the Side Lines? Not so much …

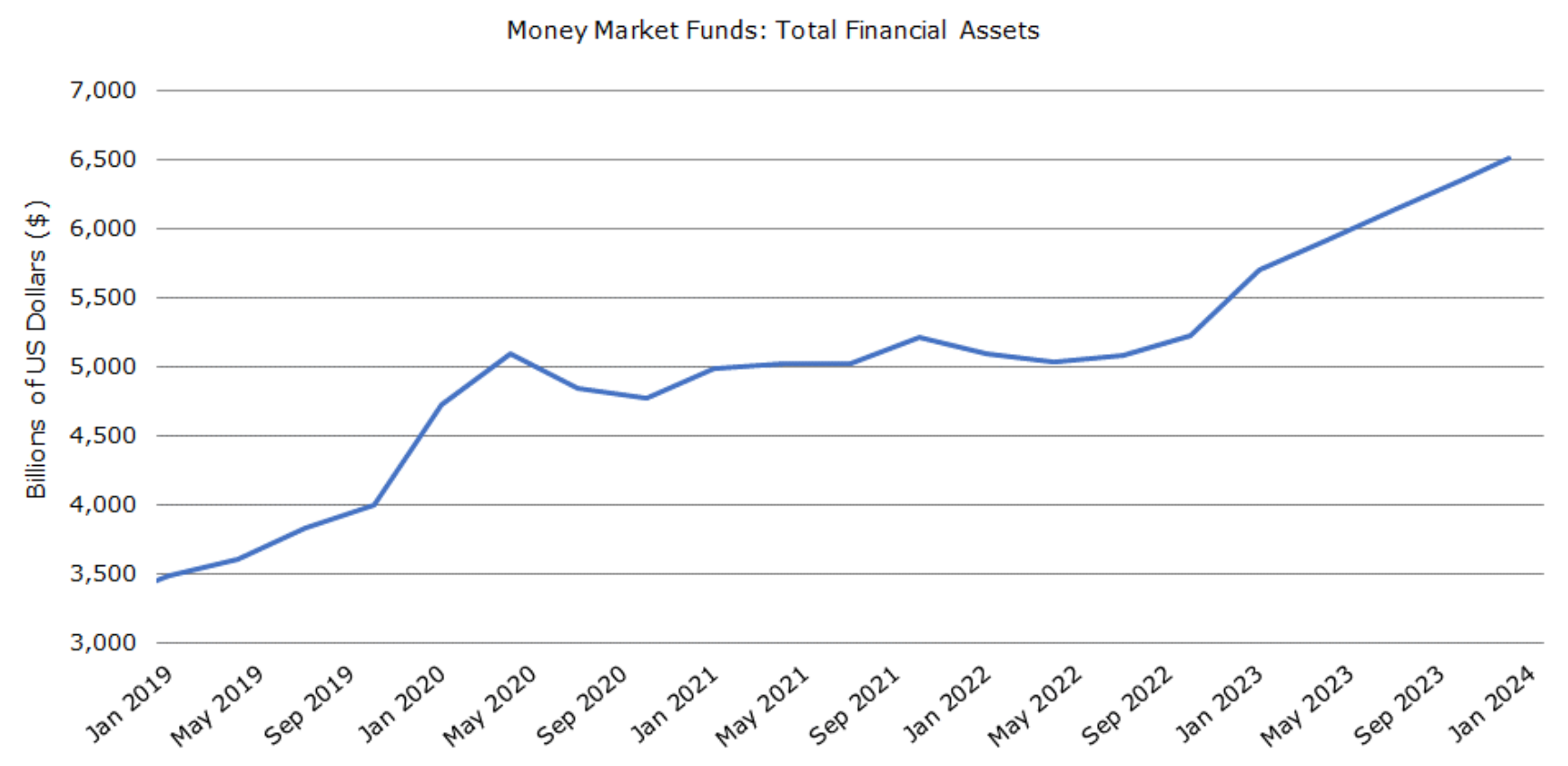

Recently there has been increasing discussion regarding the substantial amount of money on the sidelines, often referred to as “dry powder” . Some analysts point to the historically high balances in money market funds as evidence supporting this idea. However, we remain highly skeptical of the validity of this argument.

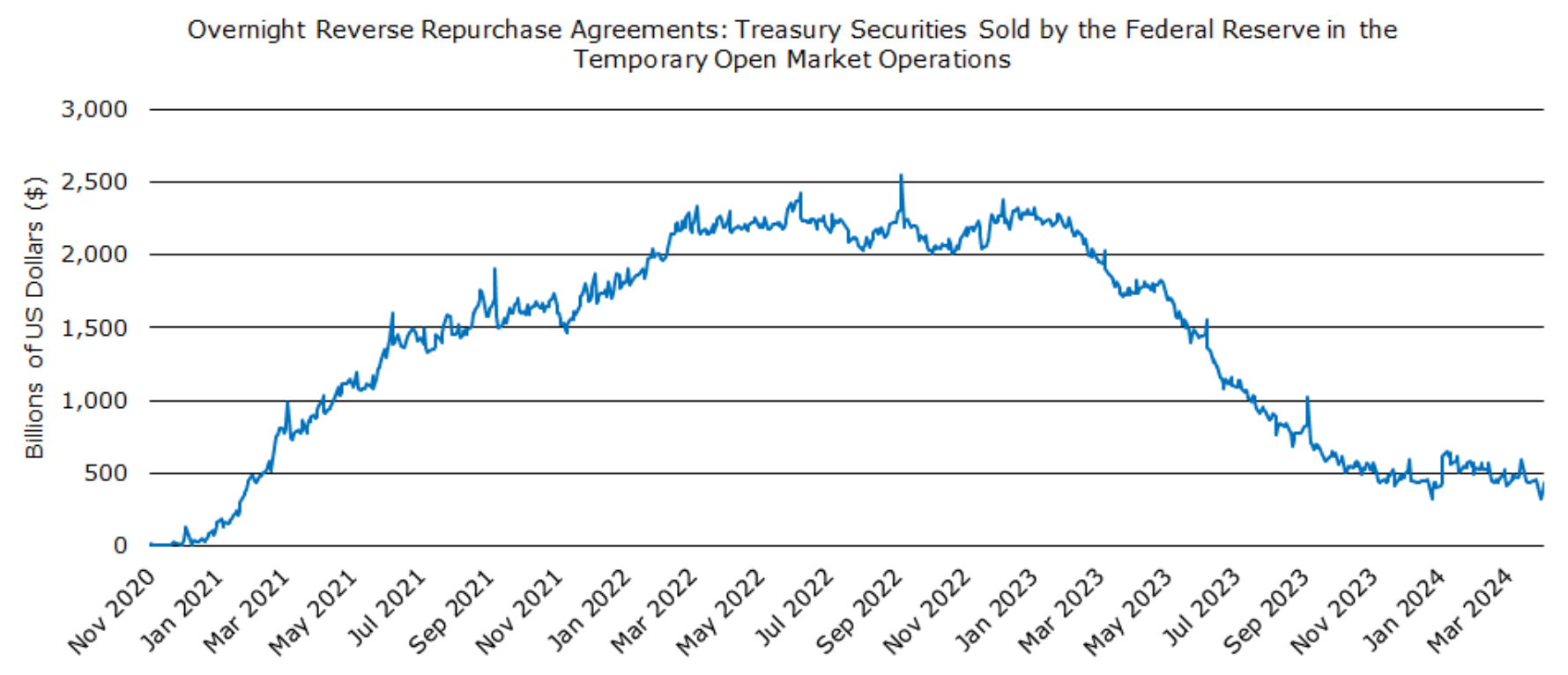

While it’s true that money market assets have reached an all -time high of $6.4 trillion, doubling since the beginning of 2019, we would contend that these funds are neither money on the sidelines nor dry powder. In explaining our reasoning, readers will appreciate our earlier diversion to discuss bank earnings. Considering the current yields on Treasury Bills, which exceed 5% risk-free, this money is less on the sidelines and more actively earning returns. Even in the event of potential rate cuts (which we believe are unlikely in the near future), investors will still seek higher returns than 5% if they move away from the relative security of money market funds. Indeed, we have to doubt that this capital will simply transition into bank deposits or a source of credit extension unless the credit yields on such investments significantly surpass current levels. At the same time, we would not expect investors to divert these funds into low-yielding asset classes. Furthermore, considering the abundant supply of T-Bills, this money, for all intents and purposes, is fully invested. This marks a significant departure from the trends of the past three decades when the outstanding balance of Treasury Bills constituted a much smaller portion of GDP. In essence, domestic financing of the federal deficit has transformed this historically significant reserve of dry powder into a more liquid asset. A more accurate metric of

dry powder, represented by funds parked at the Federal Reserve under Overnight Reverse Repurchase Agreements, has reached its lowest level in three years.

This amount, standing at $371 billion as of April 16, 2024, has plummeted from over $2 trillion less than 12 months ago, marking an 80% decline over the past year. In our view, this qualifies as a structural shift and warrants careful consideration.

Disclosures

The information contained in this document is for informational purposes only and should not be considered investment advice. This document does not constitute an offer to sell, a solicitation of an offer to buy, or a recommendation for any security or investment strategy.

Past performance is not indicative of future results. All investments carry risk, including the possible loss of principal. The views expressed herein are those of the author as of the date of publication and are subject to change without notice.

Forward-looking statements are based on current expectations and assumptions, which are subject to risks and uncertainties. Actual results may differ materially from those anticipated.

Monachil Capital Partners LP is a private investment firm. Investment opportunities described herein may be available only to qualified purchasers as defined under the Investment Company Act of 1940.