Introduction and Overview

Welcome to our February 2024 monthly report. As is our practice in these commentaries, we aim to highlight topical matters and assess their potential impact on financial markets.

In this report, we express again our concerns about the sustainability of continued economic expansion and the stability of the financial system given the high levels of deficit spending and fiscal imbalances in the US. In our view, the observed economic expansion is being fueled by government spending which continues to inflate the Federal deficit, putting it on track now to reach 7-8% of GDP.

We also examine the interaction between the Federal Reserve and the Treasury Department, and the support they are providing for economic expansion. We are deeply concerned with the accounting practices that the Fed is using to avoid recording losses on its books.

We are not doomsayers when it comes to the Treasury market as we believe the US financial system (particularly the Federal Reserve) can always support the Treasury market by issuing more currency. However, we do see that the balancing act of maintaining stability in the Fed balance sheet, supporting the fiscal expansion of the Federal government, and keeping inflation and inflation expectations anchored is gradually becoming more challenging to manage. The current trajectory will eventually force the Federal Reserve, and perhaps even the Federal Government, to make some tough choices in the years ahead.

In our view, the data illustrates that we should continue to maintain a cautious outlook when it comes to risk.

Looking into the credit markets, we are starting to see signs of irrational risk-taking in the direct lending and leverage loan markets. We believe the Fed’s reluctance to pick up the pace of its balance sheet normalization (i.e., Quantitative Tightening) is contributing to the mispricing of certain risk assets.

CPI and inflation running hotter than expected, retail sales weaker than expected

This headline succinctly captures the type of conundrum that the economy will be facing over the next few months. With federal deficit spending continuing to grow unabated, inflation is proving harder to control while the private sector is facing headwinds.

The Consumer Price Index for All Urban Consumers (CPI-U) increased by 0.3% in January, bringing the year-over-year increase to 3.1%. This caught some observers by surprise, albeit not by much, but the key trend emerging is that the path to lower inflation is proving to be more challenging than expected.

Similarly, the Producer Price Index (PPI) increased more than expected, with a 0.3% increase in January. The PPI for final demand less foods, energy, and trade services rose 0.6% in January, marking its largest advance in 12 months.

On the other side, and perhaps more worryingly, the advance estimate of US retail and food services sales for January 2024 was down 0.8% from the previous month and up 0.6% from a year ago. But how much faith should one put in these figures? We see some peril in putting too much emphasis on a single month of retail sales, as factors such as calendar peculiarities and weather can cause some noise in the monthly data.

If, instead of monthly numbers, we look at quarterly aggregate retail sales data over a 3-month period and compare it with a similar period from the prior year, we believe the analysis is better informed and less prone to measurement noise. Total sales from November 2023 through January 2024 were up 3.1% compared to the prior year. This number, in our view, is more alarming than the monthly decline because, when taken together with CPI numbers, it shows that retail sales have essentially flatlined compared to a year ago. Of course, service spending has grown and will support GDP growth. However, the overall picture does not bode very well for a balanced economic expansion.

In our view, the over-reliance of the current economic expansion on government spending is making it less robust, with inflation and higher interest rates starting to negate contributions from fiscal expenditures.

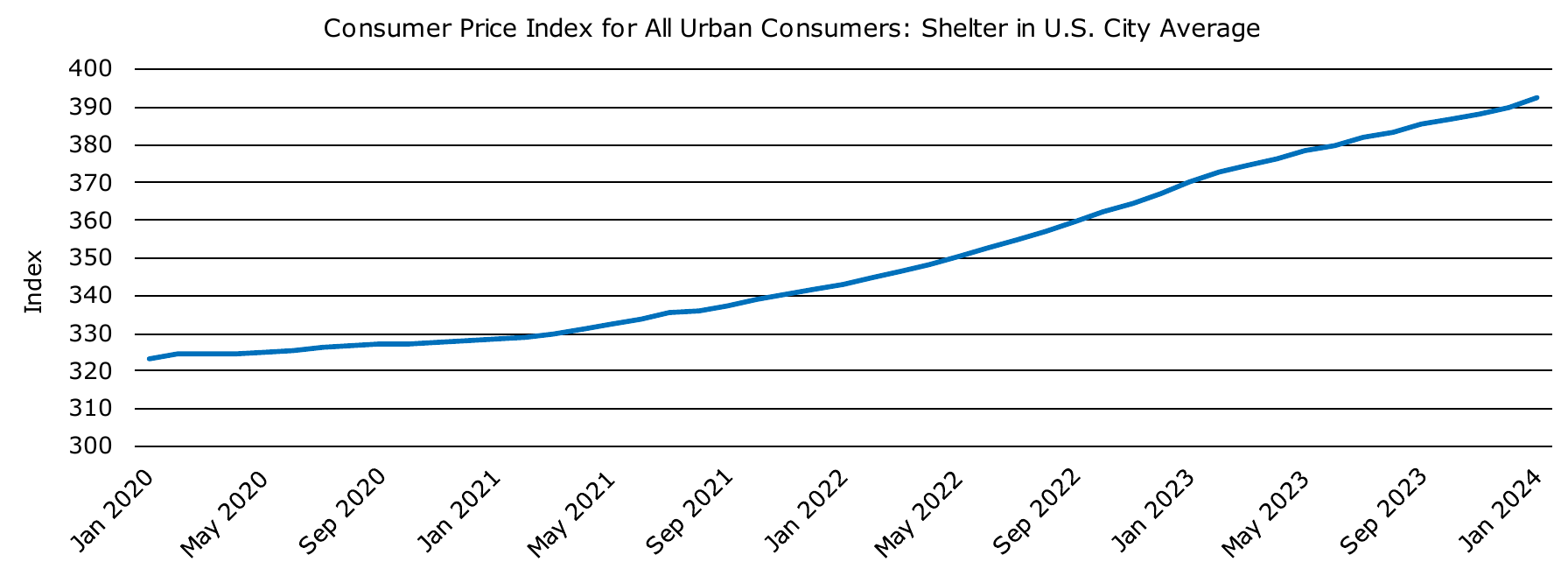

One of the most notable contributors to CPI growth in January was housing. Housing expenses (Shelter) made up roughly 36% of the CPI, with much of that coming from Rent and Owners’ equivalent rent components. The official Shelter index has grown at 6% on a year-over-year basis and, given its weight in the index, is a major driver of CPI growth.

In our view, Shelter costs will continue to remain a major contributor to inflation for the foreseeable future. Some observers have taken a benign view of Shelter inflation by pointing out that rent growth is projected to subside in the US and that the current increase in Shelter inflation is more a function of older rents being reset at the current market prices as opposed to upward price pressure on rents.

We see this explanation to be problematic on multiple fronts. First and foremost, this explanation implicitly admits that housing inflation was underreported for at least the past three years, given that the real inflation picture would have been worse if housing price increases were captured in real time. In other words, the Federal Reserve would have been even further behind the curve in its interest rate policy (even in 2023) if housing inflation had been captured accurately.

Second, changing how inflation is measured mid-cycle, and de-facto ignoring it, is not consistent with scientific integrity and rigor. Many of the people who were in the “inflation is transitory” camp in 2022 are now rushing to declare victory on inflation by disregarding the fact that the Shelter component of the CPI is catching up with reality.

Third, if one were to look at the current read of Shelter CPI, it seems that it has a long way to go before it catches up to home price increases. For reference, Shelter was

around 324 in the April 2020 Shelter CPI, and its read in the January 2024 Shelter CPI is 392 (see Figure 1). This implies a 21% increase since the onset of the Pandemic.

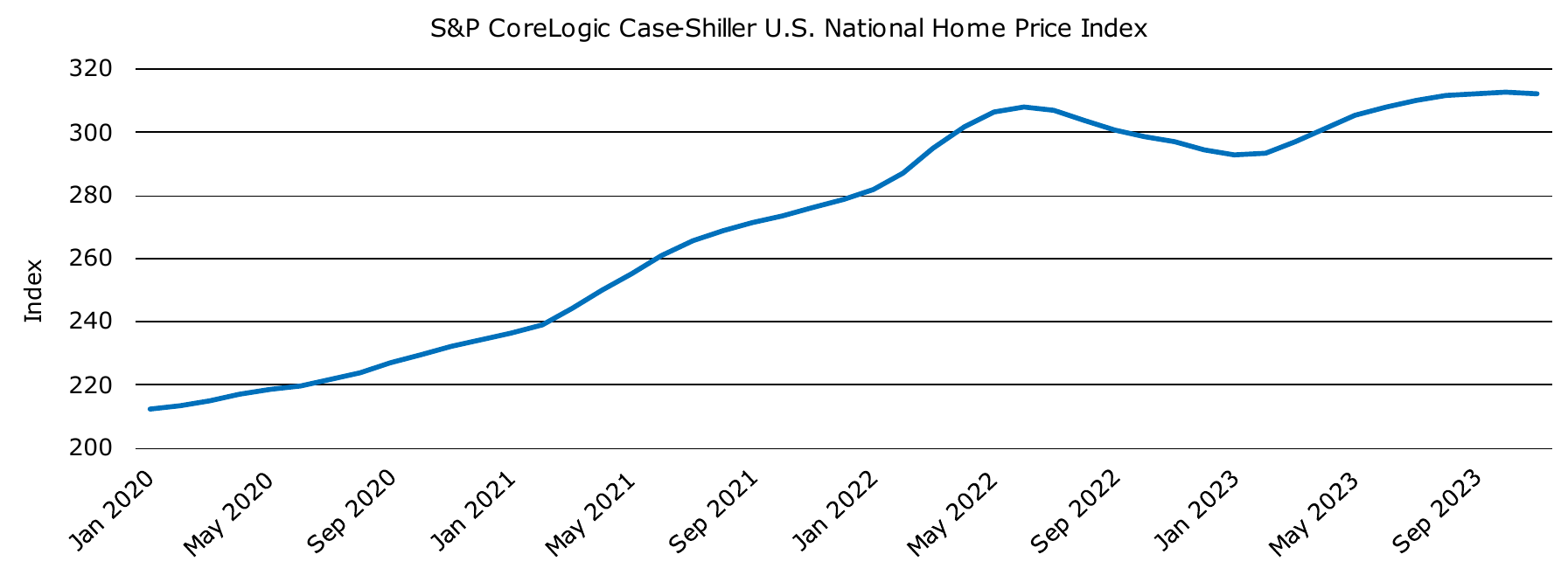

During a similar period (January 2020 to November 2023), the S&P CoreLogic CaseShiller Home Price Index grew from 212 to 312, a 46% increase, with most of the increase occurring in the first two and a half years of that period (see Figure 2).

The fact that home prices have increased 46% while the metrics that measure Shelter inflation have only gone up 21% means that there is much more catching up that needs to take place in Shelter inflation, which will invariably keep the CPI running hot for the foreseeable future.

Furthermore, the fact that interest rates and mortgage rates have increased during this period, and holding all other factors fixed, suggests that creating an equilibrium between rents and the cost of capital for housing (i.e., mortgage rates) will require rents to increase even more than home prices have. This new equilibrium can be established through higher rents, lower housing prices, lower mortgage rates, or a combination of the three. We are less sanguine about prospects of lower mortgage

rates so, in our view, a combination of higher rents (i.e. higher inflation rates) and lower housing prices are needed to achieve an equilibrium.

Federal fiscal picture continues to deteriorate, putting further pressure on economic growth

According to the Congressional Budget Office (CBO), the federal budget deficit totaled $531 billion in the first four months of the fiscal year 2024, or $71 billion worse than the same period in the last fiscal year. Adjusting for some timing shifts in outlays, the deficit would have been $80 billion, or 15% higher compared to the same period in the previous year.

While the CBO currently projects a deficit of $1.5 trillion for fiscal year 2024, we believe it is underestimating additional spending that is likely to be passed by Congress and is probably also underestimating the interest expense for Federal Debt. Our projection for the fiscal year 2024 deficit is closer to $2.2 trillion. Moreover, by not reporting losses at the Federal Reserve in the Federal budget, we believe there is at least another $100 billion of deficit spending that needs to be added to the aforementioned numbers.

Federal Reserve’s financing of past deficit spending and market intervention is causing unprecedented losses at the central bank

Another factor that is threatening the stability of the fiscal position of the United States is the real fiscal cost of current monetary policy. We believe this is a matter of major significance, even if it is neither easily grasped nor adequately reported in the financial press or other new outlets. In fact, we believe if it were reported on in a manner proportionate to its importance, it would be very prominently covered indeed.

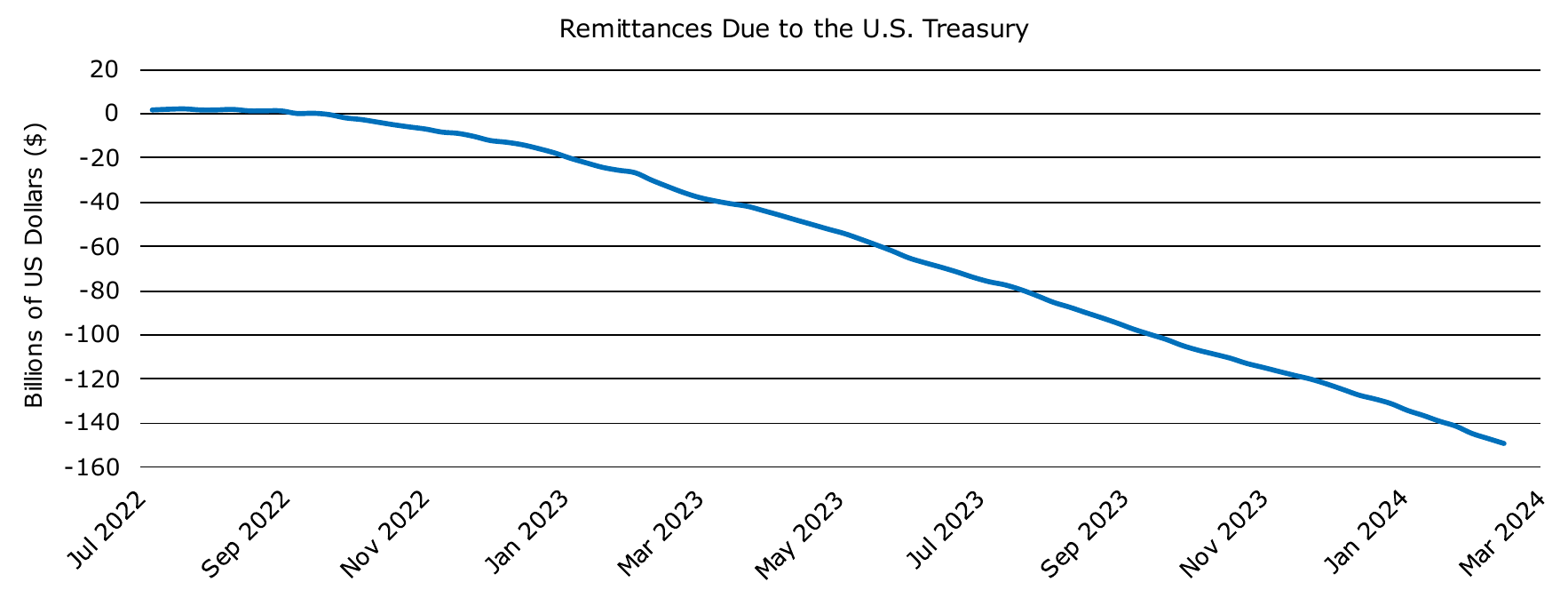

Essentially, the Federal Reserve is paying more on the liability side of its balance sheet than it earns on its assets. While fighting inflation has made it necessary for the Federal Open Market Committee (FOMC) to increase the fed fund rates, the Fed is still sitting on roughly $7.1 trillion of low-yielding Treasuries and Mortgage Backed Securities that it acquired over 15 years of quantitative easing policy. Those chickens are finally coming home to roost.

The realized losses associated with the QE policies of the past are approximately $150bn as of February 14, 2024 (see Figure 3) and currently sit on the Federal Reserve’s balance sheet

causing it to have a capital balance of ~-$100 billion.

As we first reported in our September 28, 2023 Commentary, these losses are being reported as negative remittances or negative liabilities due to the Treasury Department and excluded from the Federal Budget, which we believe is a questionable practice at best. At some point, usually, sleight of hand accounting is revealed when it collides with reality. We do not discount the real possibility that the severity of this matter could lead to the Federal Reserve requiring a bailout at some point over the next few years.

In addition, the realized losses underestimate the actual economic losses that the Federal Reserve has suffered so far. We estimate those losses to exceed $1 trillion dollars and find it likely they will continue to grow, though the actual number depends on how quickly the Federal Reserve can normalize its balance sheet.

We will continue to scrutinize the Federal Reserve’s balance sheet in our upcoming monthly commentaries.

Signs of irrational exuberance are showing up at certain corners of the credit markets

Before we close this month’s commentary, we think it is important to point out some emerging signs of irrational exuberance in certain corners of the credit markets, including private credit transactions.

We are rather alarmed by reports of banks and private credit funds competing on pricing and terms in a battle to win deals, and these reports are emerging with increasing frequency. In the past, competition among banks has resulted in the erosion of creditors’ protective rights, overleveraging in corporate debt structures, and loosening of covenants, which collectively paved the way for low recoveries and high realized losses.

This could become particularly dangerous for private lending funds if they continue to engage in this type of battle with banks over market share. We have, with some regularity, taken the opportunity to remind ourselves that sometimes it is wise and prudent to reduce risk-taking even if it means “losing out” on deals.

Disclosures

The information contained in this document is for informational purposes only and should not be considered investment advice. This document does not constitute an offer to sell, a solicitation of an offer to buy, or a recommendation for any security or investment strategy.

Past performance is not indicative of future results. All investments carry risk, including the possible loss of principal. The views expressed herein are those of the author as of the date of publication and are subject to change without notice.

Forward-looking statements are based on current expectations and assumptions, which are subject to risks and uncertainties. Actual results may differ materially from those anticipated.

Monachil Capital Partners LP is a private investment firm. Investment opportunities described herein may be available only to qualified purchasers as defined under the Investment Company Act of 1940.