Introduction and Overview

Welcome to our first 2024 monthly report. As is our practice in these commentaries, we aim to highlight topical matters and assess their potential impact on financial markets. In this report, we return to some themes that will be familiar to our readers, including the impact of federal budget deficits on inflation and 10-year yields, and their interactions with Fed policy.

We are observing three trends:

First, as highlighted in previous publications, the Federal Reserve is continuing to provide indirect financing to the Federal Government through a variety of programs including, but not limited to, the Bank Term Funding Program (BTFP). These programs are structured as implicit provisions for financing holders of government securities rather than requiring that they become direct purchasers. Despite this trend, the spread between yields on government securities and the cost to finance government securities continues to expand, thus demonstrating the scarcity of the Federal Reserve’s balance sheet.

Second, despite the Fed’s best efforts, measures of excess liquidity in the financial system—including the size of the reverse repo facility—continue to decline. This should not be surprising as the quantum of the Federal budget deficit is significant by any historical measure. Absent a material change in the Federal Reserve’s policy framework, we expect the reverse repo facility balance to approach zero by the end of Q1.

Third, inflation continues to remain stubbornly high. While we are seeing some declines in measures of inflation, the most recent inflation reading portends a path to 2% inflation that is much longer than many observers continue to expect, or at least profess to expect.

As a result of these trends as well as the growing Federal deficit, we continue to remain very skeptical of the prospect for a soft landing. In our view, given the recent rally in the public credit markets, there is currently limited excess value in public transactions. This is an observation that we continue to incorporate into our portfolio selection and our credit decisioning.

Inflation continues to remain well above the Fed’s stated target rate

The Consumer Price Index (CPI) increased 0.3% in December, following a 0.1% increase in November. Furthermore, over the last 12 months, the index has increased 3.4% despite the energy index having dropped 2% during that same period. Excluding food and energy, the index actually rose 3.9% over the past 12 months.

Much of the increase was owing to the 6.3% YoY increase in owner’s equivalent rent (cost of housing), which represents roughly 25% of index. The surge in this expense highlights the toll that housing inflation had on the consumer in 2023. We expect this number to remain high as much of the impact of recent housing inflation will not have been fully captured in the CPI number.

There were two interesting outliers in the CPI report. The first being Health Insurance, which was reported to have declined by 27.1% year-over-year, and the other being Motor Vehicle Insurance which was reported to have had a YoY increase of 20.3%. I have observed anecdotal evidence of the increased cost of vehicle insurance, so am not surprised at data that substantiates it. I am, however, skeptical about the reported decline in the cost of health insurance. To be clear, the manner in which health insurance costs have been measured and reported over the last several years invites suspicion. In particular, this figure’s calculation touches various components including, for example, what consumers pay vs. what employers pay, and how the employer contribution is measured as employment cost vs. consumer inflation. To me, there is a lingering concern that this morass of variables could present an interesting opportunity for an enterprising economist. In any event, one has to wonder what could explain such a precipitous decline.

Nevertheless, we believe the “last mile” for reducing core inflation from 3.9% to 2% will be a very rough road that will require the Federal Reserve to maintain significant discipline to avoid repeating mistakes of the past. The question remains: “What will be the real world and market implications of having an inflation rate that remains stubbornly above 3%?” We believe that private purchasers of long-term government bonds (especially households and foreign purchasers) are going to demand higher returns as holders of US government obligations.

Excess Liquidity in the Financial System Continues to Decline:

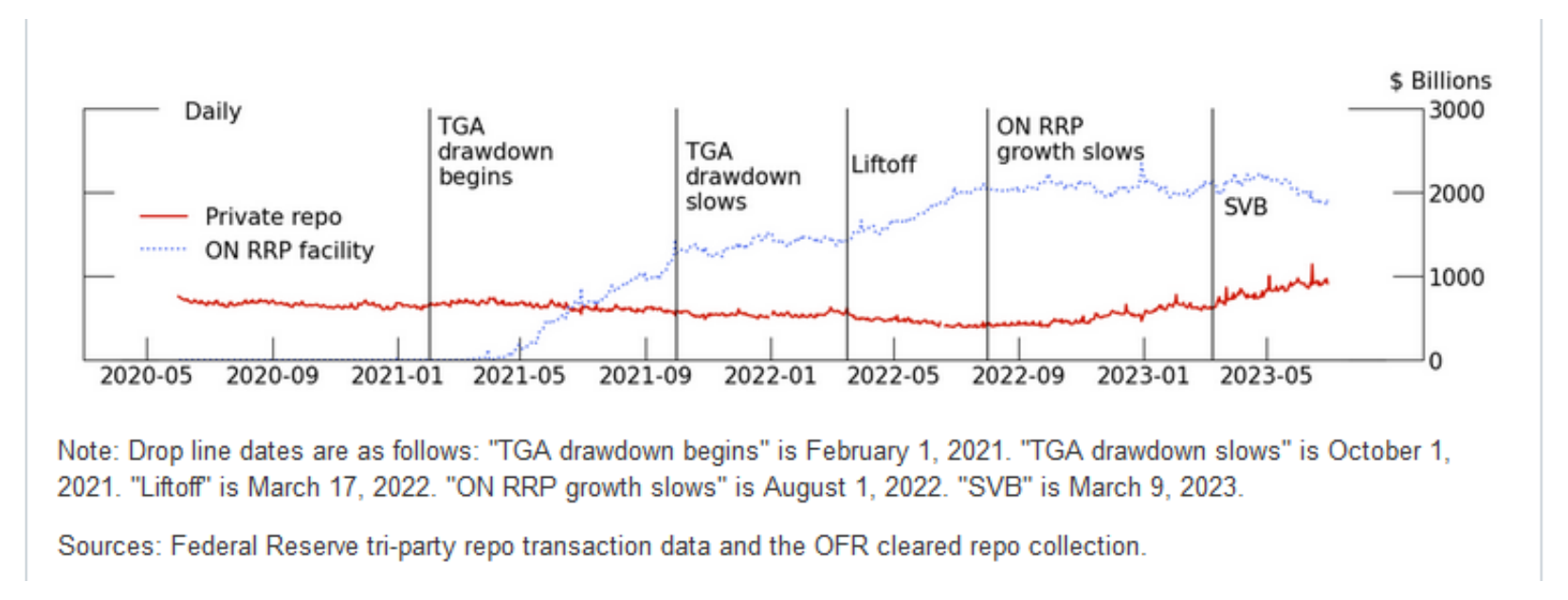

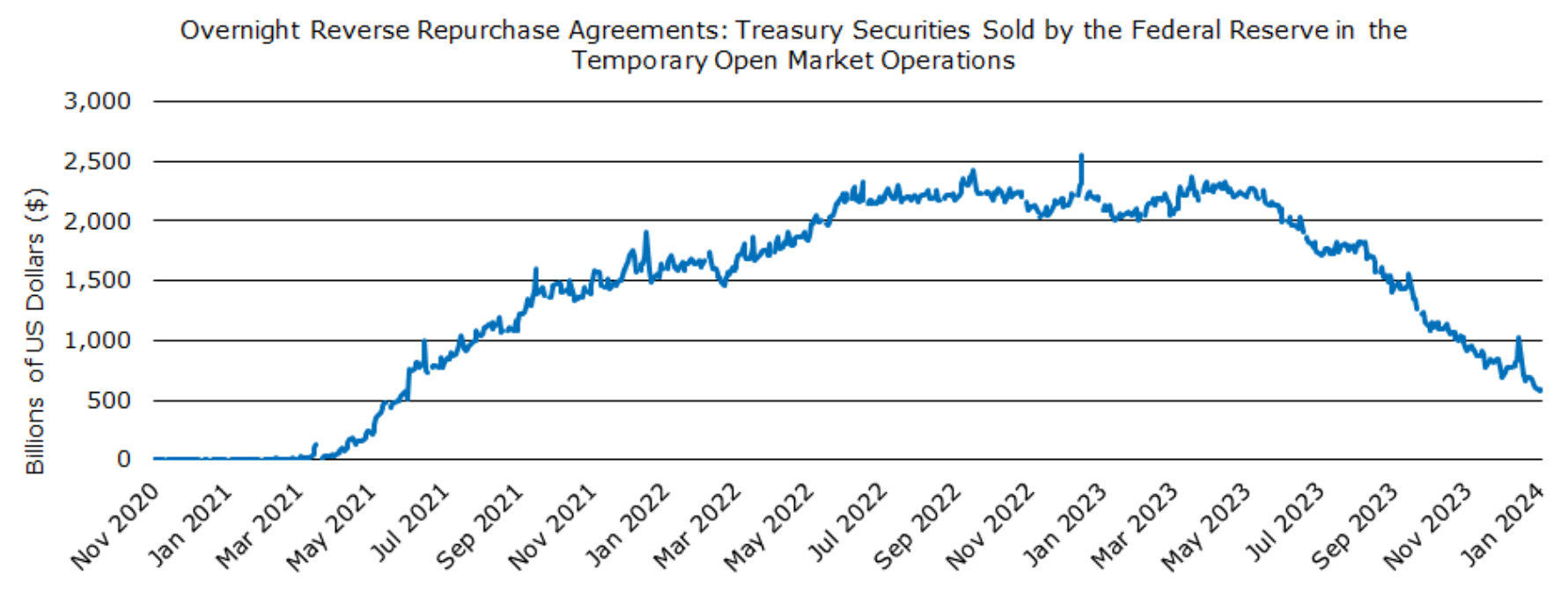

At the same time, measures of excess liquidity in the financial system continue to decline. Our favorite metric for measuring excess liquidity is the take-up of the Federal Reserves’ Overnight Reverse Repurchase (ON RRP) facility. This was catalyzed by the biggest source of take-up (i.e. the largest users)—Money Market Funds (MMFs). In the aftermath of fiscal expansion in 2021, excess liquidity from federal deficit spending combined with a Zero Interest Rate Policy (ZIRP) created excess liquidity for MMFs, driving them, as well as some other financial institutions, to be parked with the Fed under the ON RRP facility.

During recent months, however, particularly following the extension of the debt ceiling which gave the treasury unlimited borrowing authority until 2025, increased borrowing by the government has caused the size of the ON RRP facility to rapidly shrink, as

illustrated in Figure 2 (below). It is specifically notable that, since the resolution of the debt ceiling in June 2023, the size of the ON RRP facility has declined from ~$2.2 trillion to ~$590 billion as of January 17, 2024.

It could appear as if MMF took the money placed with the Fed to absorb the wave of the treasury issuance after June 2023.

In light of the continued growth in the federal deficit, and absent a dramatic change in the Fed’s monetary policy stance, we expect the ON RRP facility to continue its decline and to reach near-zero by the end of Q1 2024.

Given the MMF’s role in private repo markets, it is also possible to observe some structural changes over the next several months, including more scarcity, tighter margin terms, and increased price movement.

Federal Budget Deficits, as the driving force behind the supply of Treasuries, are expected to continue to expand

On January 9, 2024, the Congressional Budget Office published its Monthly Budget Review for December 2023, covering the first quarter of fiscal year 2024 (OctoberDecember 2023). The first quarter came in at a deficit of $509bn, an increase of 21% from the same period in the prior fiscal year. In our view, the full year deficit is now tracking at $2.2-$2.5tn, which will be close to 8% of GDP. The federal government’s need to finance this level of deficit spending will continue to be a major driver of financial markets, given that it will force the federal reserve to either accept higher long-term interest rates (meaning it tries to fight inflation by limiting its balance sheet) or, alternatively, to accept higher inflation. We can only hope that they have the wisdom to understand that using the Fed’s balance sheet is not a sustainable solution.

Federal Reserve continues to provide direct and indirect financing to the Federal government.

While official Federal Reserve policy states that it is engaging in quantitative tightening (QT), the reality has been a program of backdoor quantitative easing (QE). One of the

mechanisms to achieve this has been support for the Repo market through the banking system. Let’s consider this briefly.

The end users of the repo market typically use repurchase agreements to leverage their holdings of government securities, sometimes as much as 50-to-1. As such, a relatively small pool of capital can suddenly create demand for a large quantity of Treasuries. For example, by using repo financing for leverage, a $1bn pool of capital can be used to purchase as much as $50bn of treasuries. By supporting and encouraging banks and financial institutions to use repos, the Fed can significantly increase demand for treasuries.

That encouragement can be achieved through a myriad of tools available to the Treasury. The Federal Reserve can, for example, backstop repo transactions or provide repo financing to banks. So, while the Fed is technically neither buying treasuries nor engaging in QE, it can almost directly provide financing to the Federal government.

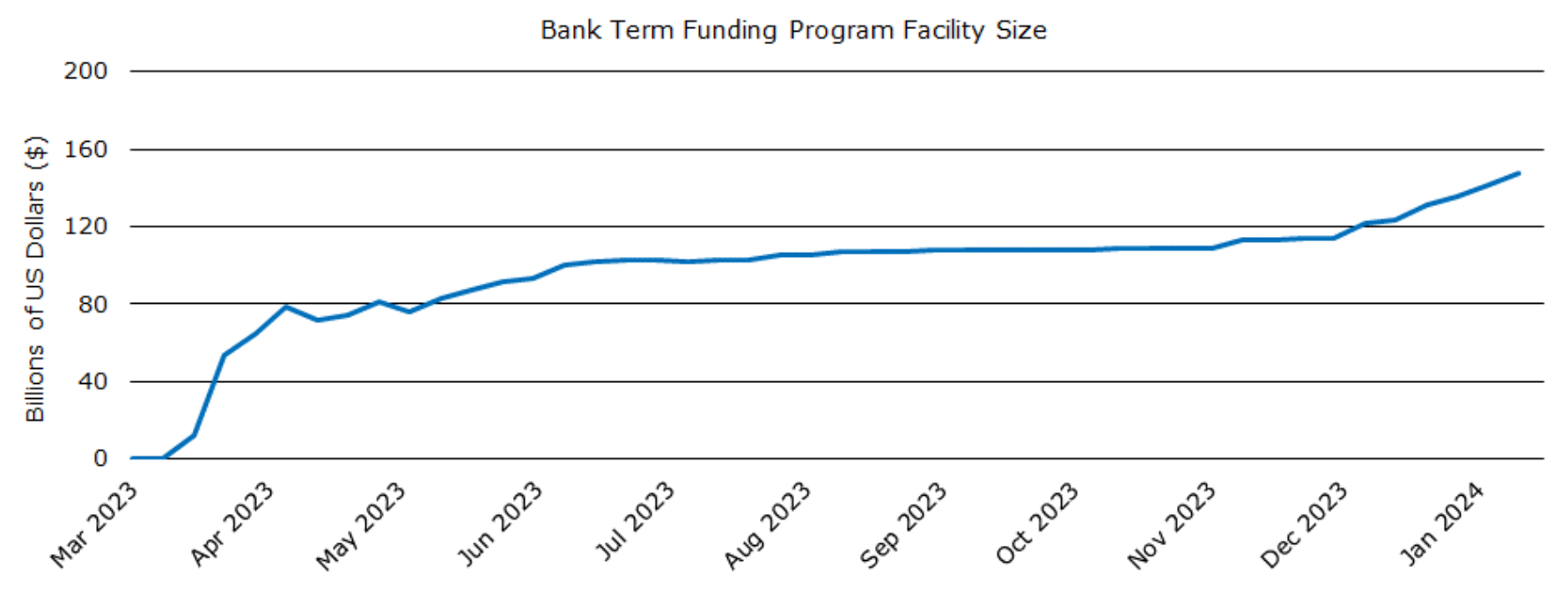

One of the programs employed by the Fed is the Bank Term Funding Program (BTFP). This facility provides banks with the ability to borrow money at 1-year the Overnight Index Swap (OIS) rate + 10 bps. The Federal Reserve is essentially providing oneyear repo financing with a 100% advance rate secured by US Treasury instruments.

As a further incentive, the program is not subject to any prepayment penalties. For some enterprising banks, this program has become a federally funded goldmine. They can simply finance their treasury holdings with the Fed at a relatively low rate and deploy their borrowings while achieving returns far in excess of 1-year OIS + 10 bps. Given that 1-year OIS is at 4.73%, the cost of utilizing this financing is much lower than the current short term repo rates. Essentially, banks can obtain 1-year funding from the Fed with full prepayment optionality at a much lower rate than the one they can turn around and earn in the repo market. That condition has opened up a significant arbitrage opportunity for banks and has increased the take-up of the BTFP.

In our view, part of the issue with all of this is that rather than serving as an emergency facility (which incidentally should have a relatively high cost associated with it), the BTFP has become a “cheap” source of financing. In essence, the Federal Reserve has gotten into the business of lending money, with full prepayment optionality, at levels tighter than its stated policy rate of 5.25%. One could argue that this program actually has the function of a rate cut.

Despite the Fed’s unprecedented liquidity programs, signs of stress are appearing in the Treasury Market

While the Federal Reserve’s balance sheet continues to expand and funding continues to be made available to banks at very attractive levels, signs of stress are appearing in the Treasury Market. The spread between treasury yields and the SOFR swap rate (e.g. 10-year treasury yields over 10-year SOFR swaps) continues to grow. This spread, or basis, has widened from 15 bps in February 2021 to a current level of 38 bps, one of the widest on record.

We expect this basis to continue to widen as the supply of treasuries continues to increase while balance sheet capacity to hold them remains constrained.

If the Fed continues to embark on policies designed to create balance sheet capacity at tight pricing for Treasuries, it will inevitably make its campaign to reduce inflation less effective.

Market Opportunities and Outlook

In our view, the recent rally in the public credit markets is overdone and we believe the pendulum is swiftly swinging in the direction of relatively more value being available in private markets. While we had increased our holding of public credit instruments (mainly ABS) in the aftermath of spreads widening in March 2023, we now expect our portfolio to shift towards holding more privately negotiated transactions.

Disclosures

The information contained in this document is for informational purposes only and should not be considered investment advice. This document does not constitute an offer to sell, a solicitation of an offer to buy, or a recommendation for any security or investment strategy.

Past performance is not indicative of future results. All investments carry risk, including the possible loss of principal. The views expressed herein are those of the author as of the date of publication and are subject to change without notice.

Forward-looking statements are based on current expectations and assumptions, which are subject to risks and uncertainties. Actual results may differ materially from those anticipated.

Monachil Capital Partners LP is a private investment firm. Investment opportunities described herein may be available only to qualified purchasers as defined under the Investment Company Act of 1940.