AUGUST MARKET AND ECONOMIC INSIGHTS

September 2023

Introduction and Overview

Welcome to the August installment of our monthly report, where we aim to highlight topical matters and assess their potential impact on financial markets.

We will begin by revisiting the markets and pundits’ continued desire to believe in a soft landing. As you will be aware from our previous commentaries, we have been highly skeptical about the likelihood that the US economy will enjoy a soft landing. Our point of view has not changed. In this report, we explain the reasons behind our skepticism and describe the framework for our analysis.

Proponents of a soft-landing point to data ranging from GDI/GDP to labor market indicators to make their case. Holding aside the questionable quality we consider to be inherent in this data, we believe it is simply premature at this point, and most likely inaccurate, to declare that a soft landing has already occurred.

Imbalances in the markets for saving and investments make a soft-landing extremely unlikely

Our approach for creating a robust framework for considering the soft-landing narrative is based on Karl Popper’s view that a valid scientific thesis requires falsifiability. (For our more curious readers, we suggest reading the philosopher’s book titled “The Logic of Scientific Discovery”.) In this vein, we will present a set of measurements and conditions that, if met, would be acceptable as a refutation of our thesis, i.e., that a soft landing has not, and will not, happen.

The popular soft-landing narrative is that the recent reduction in inflation, combined with job growth and positive GDP, together indicate that the markets for goods and services are finding equilibrium, i.e., that the signature feature of a soft-landing has materialized. In our view, this narrative omits the growing disequilibrium in financial markets, which generally achieve equilibrium through the mechanisms of interest rates and risk premiums. We do, however, think that:

A) Equilibrium in the financial markets following the increase in interest rates has not been fully restored, due, in part, to distortions caused by the Fed ’ s Treasuries holdings and other types of credit extension. B) Neither households nor corporates have yet to fully adjust their savings, consumption and investment behavior based on higher interest rates.

Until both of these factors reach their steady state, the economy cannot reach one. In our view, that steady state may include lower growth (due to higher interest rates) and higher inflation (due to even greater deficit spending).

Deficit spending is pushing interest rates higher

Increasing governmental deficit spending is stimulating demand from the federal government for investments. This increase in demand is pushing long-term interest rates higher which, in theory, should push down consumption as households will have an incentive to save more. Essentially, higher interest rates are the mechanism by which capital markets can reach equilibrium and where household savings become an increasing source of financing government deficit spending.

Higher interest rates would reduce demand and private sector investments

Higher interest rates are likely to have two profound impacts on the private sector economy, each of which we see as reducing demand through a variety of mechanisms. First, as the cost of borrowing increases, consumers are less likely to use credit to finance their purchases and consumption. Second, the incentive to save increases as higher returns on debt investments become available in capital markets.

Of course, higher interest rates — especially in longer term investment products — are purely a monetary manifestation of what is happening in the markets for goods and services. As government deficit spending creates demand, that demand needs to be balanced by higher rates of savings and less consumption by households, with higher rates serving as the financial market mechanism that provides for this new equilibrium.

Similarly, as longer term rates rise, opportunities for private sector investments will be reduced. Projects that may have been viable at a lower financing cost become less viable and therefore unavailable as an investment opportunity.

Impact of higher interest rates has not yet fully transitioned into the broader economy and financial markets have not yet fully priced them in

We believe we are still in a honeymoon phase, where government spending has created a short-term boost to GDP without, as previously discussed, a commensurate boost to GDI or higher interest rates fully impacting demand. Specifically, in the US, although GDP growth has been fueled by deficit spending, lower household spending has not yet fully materialized.

Long term rates are reaching record highs

Long-term US interest rates, particularly the 10-year, have recently reached their highest levels in 15 years. This is largely driven by increasing issuance by the US treasury, which is required to support the ever-expanding government deficit.

As we have postulated in prior reports, current inflationary pressures are simply too strong and too embedded within the economy for a recession alone to reduce them. As such, the Fed is left with limited room for an effective monetary policy easing.

We remain highly suspicious of the recent rally in the financial markets, which is far broader than the oft-discussed AI frenzy. In our view, this movement is a byproduct of a monetary policy that is just not tight enough. While the Fed has officially begun Quantitative Tightening (QT), it is our observation it has concurrently provided credit beyond the remit of the " neutral " central bank. The Federal Reserve has, for example, provided credit to finance banks covered by FDIC. In our view, such credit extensions have the monetary impact of countering the intended effects of QT by having the Fed effectively finance illiquid — and often low quality — bank assets.

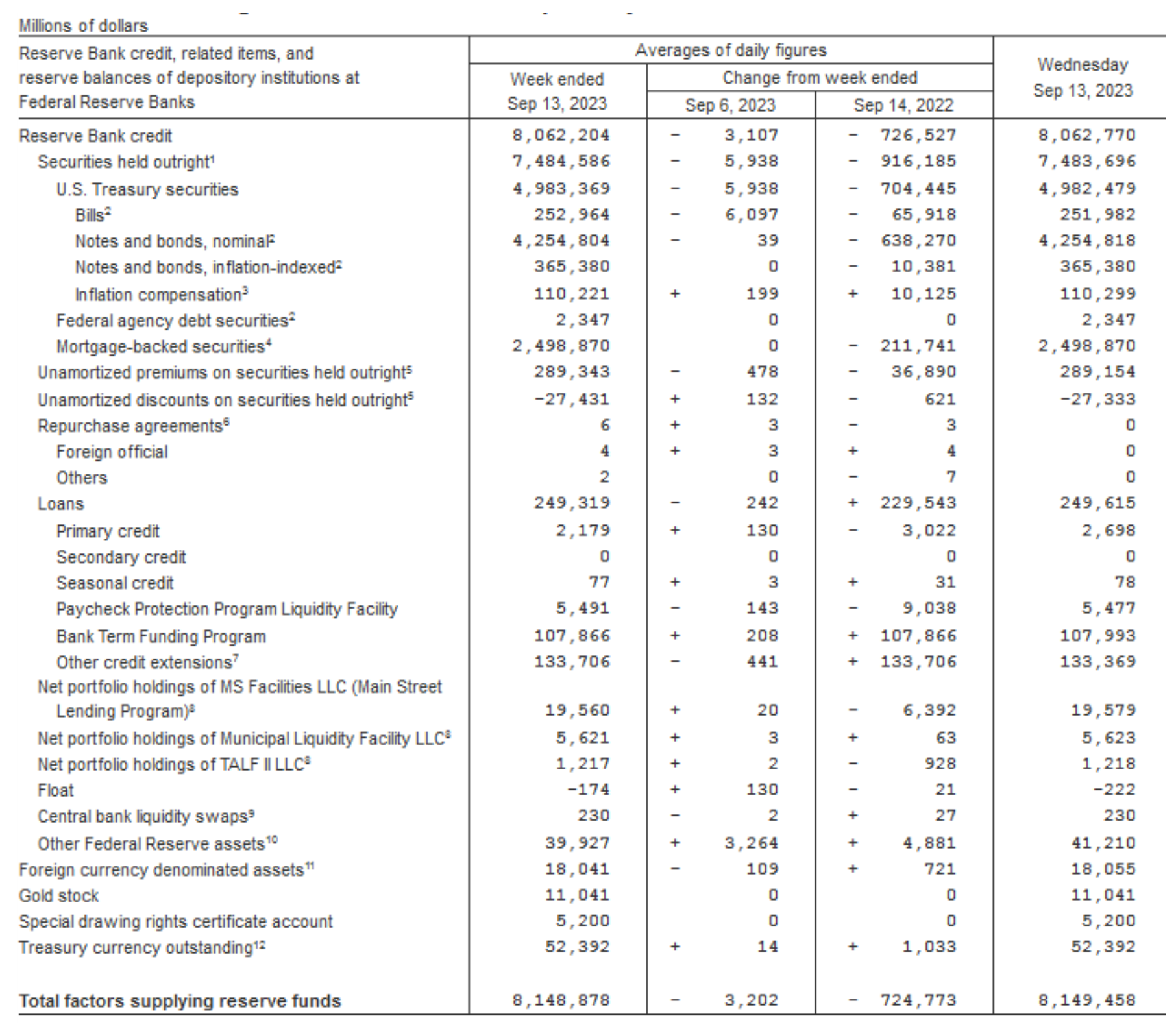

Combining this observation with the fact that Fed still holds $7.5 trillion of Treasury assets (see Figure 1), we believe it is certainly arguable that Fed is continuing to provide significant support to financial markets.

The Fed itself has suffered significant losses in its treasury holdings and is employing questionable accounting practices

The previously employed Quantitative Easing (QE) and the subsequent round of QT have not been without their costs. Specifically, we question why prior to initiating the current QT the Fed opted against beginning to unwind its balance sheet more quickly while also normalizing asset holdings rather than hastily (in our view) increasing rates. Is it possible that they were afraid of the political consequences of a steeper yield curve and higher mortgage rates? That question is more likely to be answered by financial historians than within the confines of this piece.

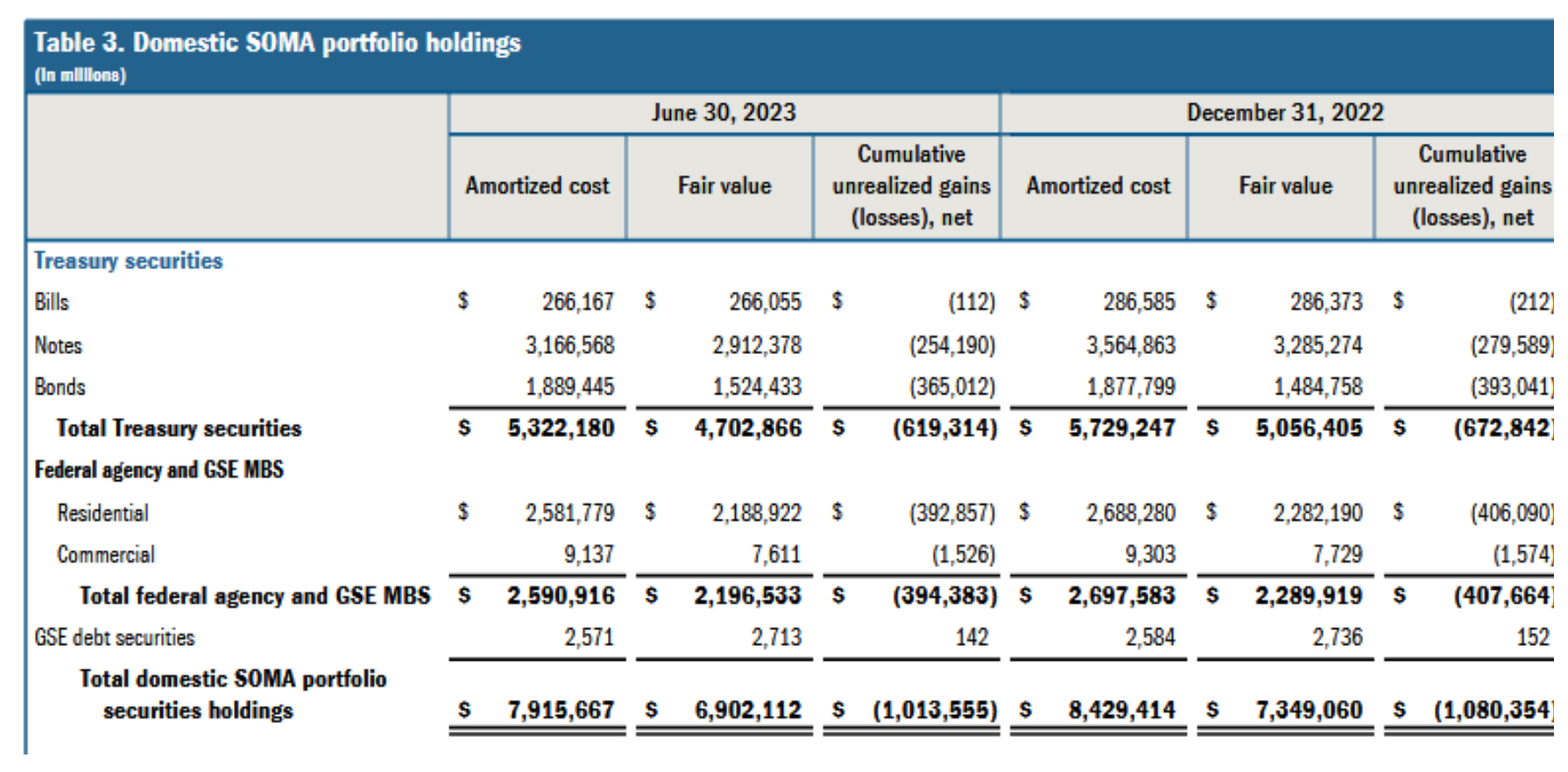

Nevertheless, we believe this fateful decision by the Fed has had material adverse effects on the health of its own balance sheet. For example, mark-to-market losses

taken by the Fed, which they report as “unrealized losses , " ha ve recently exceeded the $1 trillion dollar mark.

The Fed does not report these losses as a “mark down” of its balance sheet, but instead discloses them only as supplemental financial information, a tactic akin to the standard of practices at Silicon Valley Bank.

The specific nature of these losses can be traced to Fed purchases of treasuries at very low yields in order to support QE. With market yields now having moved much higher, those purchases are underwater.

Although the Fed does not recognize these losses on a current, fair value basis, they are gradually being realized. Given the current rate environment, Fed outlays on its deposits and liabilities far exceeds what it is earning on these lower yielding assets. Supporting a balance sheet with a current cost 5.25%-5.50% by holding treasuries that are yielding 2% will inevitably, and continually, create losses. In fact, for the first 6 months of 2023, the Fed has realized ~$53bn of losses related to this differential, and that is before accounting for its operating expenses which, when included, bring losses to ~$57bn. Despite all of this, the Fed has reported positive comprehensive income in its most recent quarterly report.

How are they bridging the gap between these losses and positive income? They are employing what we believe is a questionable, albeit clever, accounting trick in which they offset these $57bn of losses with a negative $58bn of remittances to Treasury. Essentially, they are creating an accounting construct from the Treasury without it being recognized as a Treasury obligation. Furthermore, we expect these “negative remittances” , or misclassified receivables eligible for offset by future obligations, to continue to increase and, given the current interest rate environment, we see as exceeding $1tn over the next few years.

Interestingly, the CBO in its most recent monthly budget review, simply states that Fed remittances to the Treasury are “… less than $1 billion so far this year …” without making references to the fact the Federal Reserve is actually recording a negative reserve.

At this point, not only is the Federal Budget not on a sustainable path, but the Federal Reserve has unrecognized losses that exceed its capital base and, in our view, is using accounting trickery to obfuscate it. The magnitude of these losses could eventually exceed $1 trillion and will ultimately need to be absorbed by either the banking system or the Treasury department.

We are not close to a soft landing

So where are we now? We see the economy in a state characterized by:

- Inflation that slowed down due to short term factors but is reaccelerating. • Economic growth that, on the surface, looks healthy but is dependent on Federal Government deficit spending. • An unsustainable Federal budget that needs to reach a stable path either through higher taxes or lower spending. • A central bank balance sheet that is insolvent on a fair value basis with even realized losses not being recorded as losses.

We believe this image is inconsistent with the picture of an economy about to have a soft landing.

What would a soft landing look like?

In our view, to achieve a soft landing, we would need to have the following factors simultaneously present in the economy:

- Low inflation (probably at 2% or less) • Economic growth shown as growth in both GDP and GDI • Stability in budget growth, with sustainable debt load and a sustainable deficit (probably at around 3% of GDP) A sustainable central bank balance sheet, where losses are absorbed by the • taxpayer

If these conditions were to be achieved, we would accept that the Fed has achieved a soft landing. With many of these conditions currently outside the Fed’s control, and even considering those with in the Fed’s control, the Fed’s practices have been questionable at best — and extremely costly at least.

Disclosures

The information contained in this document is for informational purposes only and should not be considered investment advice. This document does not constitute an offer to sell, a solicitation of an offer to buy, or a recommendation for any security or investment strategy.

Past performance is not indicative of future results. All investments carry risk, including the possible loss of principal. The views expressed herein are those of the author as of the date of publication and are subject to change without notice.

Forward-looking statements are based on current expectations and assumptions, which are subject to risks and uncertainties. Actual results may differ materially from those anticipated.

Monachil Capital Partners LP is a private investment firm. Investment opportunities described herein may be available only to qualified purchasers as defined under the Investment Company Act of 1940.