Introduction and Overview

Welcome to the July installment of our monthly report, where we aim to highlight topical matters and assess their potential impact on financial markets.

In a recent event that should have come as a surprise to no one, Fitch Ratings downgraded the US Treasury’s Long-Term Issuer Default Rating from AAA to AA+, a move that has elicited much commentary from market participants. In our view, persistently increasing levels of deficit spending by the federal government, compounded by lower-than-expected revenues, provide a well-justified basis for this credit downgrade. In fact, as we will discuss in more detail, it is our view that some of Fitch’s budget and spending assumptions are optimistic, making further downgrades a distinct possibility.

We will also discuss Q2 2023 GDP data in the context of a theme in last month’s letter, namely how varying degrees of lags and delays can impact reported figures and add nuance to the interpretation of economic data. This condition is particularly acute when considering factors impacting inflation, ranging from the war in Ukraine to the effects of the aforementioned deficit spending by the US government. As a case in point, we are seeing evidence that reduced growth in CPI was due, in part, to short-term transient factors, including initial commodity price shocks and subsequent moderation in the aftermath of the release of the Strategic Petroleum Reserve (SPR). In our view, the CPI may well start to tick up from this point.

We also note that GDP growth for Q2 was underwhelming at best (due again in part to ever-increasing levels of government deficit spending), and that the gap between GDP and Gross Domestic Income (GDI) is widening ominously. Historically, GDI and GDP trend in the same direction, which one would expect since they both measure economic output, and GDI generally hovers slightly above GDP in absolute dollars. In recent quarters, though, GDI has crossed below GDP. We believe this supports a higher likelihood of recession as the only time this has happened in recent history was ahead of the Great Recession of 2008 and (briefly) during 2020.

A final worthwhile observation from the dataset available in July came in the form of earnings reported by banks, and regional banks in particular. Amongst several takeaways, we note that although banks in general have access to deposits, the cost of those deposits continues to be on the rise.

Inflation and growth measurements continue to be impacted by data lags and uncertain cycles.

The CPI reading for June 2023 released on July 12 showed a YoY increase of 3%, one of its lowest readings since March 2021. We believe the ensuing applause for these low levels of CPI growth was premature if not entirely misguided, and that there are factors impacting the calculation of these CPI numbers that call for careful consideration. These outside forces vary in timing and severity but include, in our view, the war in Ukraine and its impact on energy and commodity prices, the overall level of US deficit spending, and government policies mandating transitions from cheaper sources of energy.

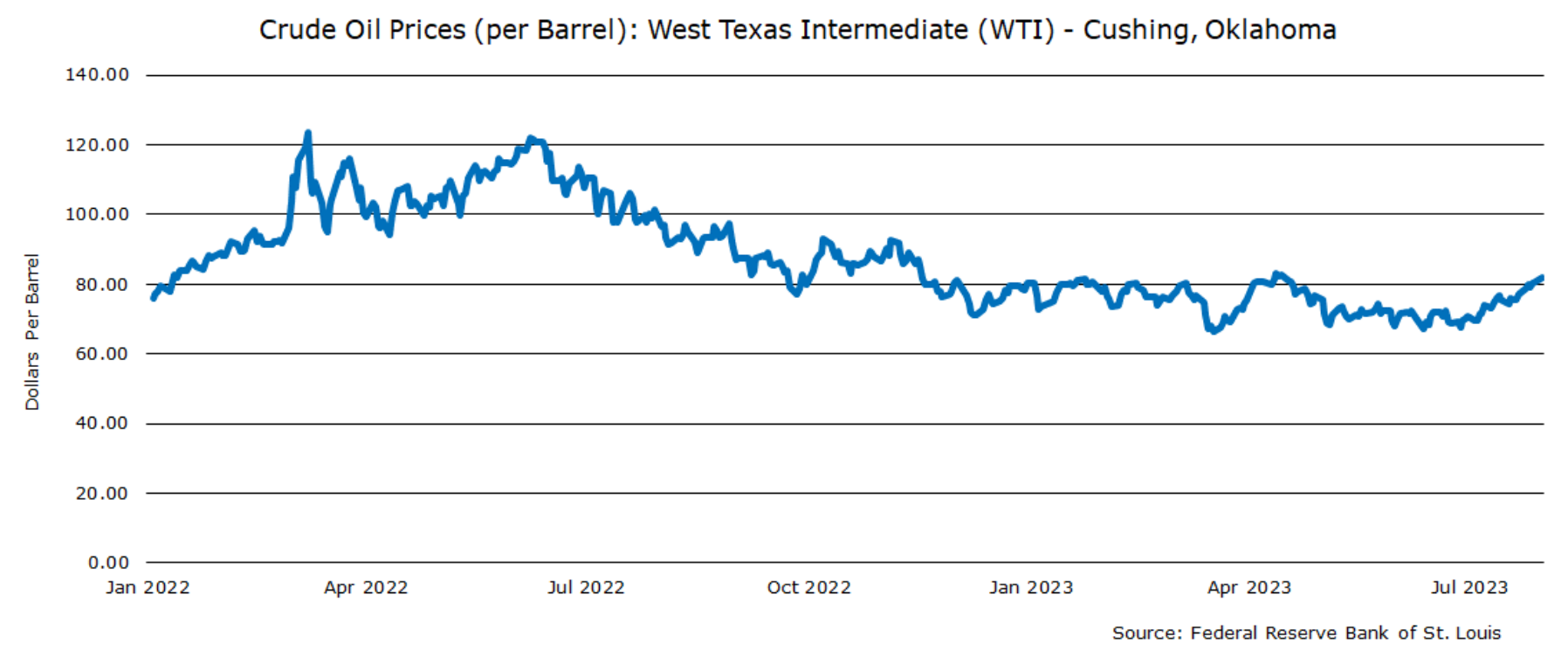

Energy prices, for example, initially spiked following the onset of the war in Ukraine, causing CPI to quickly move higher, eventually peaking at a 9.1% YoY growth in June 2022. Subsequently, following a period which included ineffective Western sanctions on Russia and the draining of the SPR, energy prices collapsed with oil prices bottoming out at ~$67 in June 2023. It is worth noting that oil prices rebounded in July to above $81 and have generally stayed above the $80 mark since then. Figure 1 details this price movement and its impact on inflation by illustrating how price increases in early 2022 were followed by a sell-off in late 2022 and early 2023. This has resulted in a lower reading for inflation than had been recorded in some time.

These significant moves in both directions occurring within a 16-month cycle are a direct impact of the war in Ukraine. It would be extremely premature, however, to interpret the war’s impact on energy prices as a sign of victory in the Fed’s fight against inflation.

In assessing the impact of outside forces on economic data, it is useful to consider what we call the “lag”, i.e. how immediate does the factor affect the data, and its “lifecycle”, i.e. how long will the factor persist in affecting the data. In the case of the Ukraine war, we see this as having both a short lag and a short lifecycle. Other factors manifest more subtly with longer lags but also have longer lifecycles, from which it follows that they will have a more prolonged impact. These other drivers include, but are not limited to, increased demand, the crowding out of private investment and diminished economic capacity, all of which are instigated by government deficit spending and government policies/legislation that create artificial incentives, of which the so-called “Inflation Reduction Act” is a prominent example.

Increases in government deficits and spending are both also inflationary, but with some nuanced differences between the two. Increases in government deficits — particularly if accompanied by central bank monetization of government debt — drive inflation by increasing money supply. Increases in government spending, on the other hand, tend to be indirectly inflationary due to the reduction in productive capacity resulting from government inefficiencies while allocating capital. In short, increased deficits and spending tend to bring on longer cycles with much longer lags.

While a war could create an immediate supply disruption, and failed sanctions and SPR releases can reverse the impact of said disruptions, changes in government policy towards more expensive sources of energy, as well as increases in government spending and deficits, will take some time to show their full effect.

In our view, we currently reside in an “artificial sweet spot , " w here inflation measures are temporarily cooling and increasing government spending is temporarily pushing GDP growth numbers higher. We believe, however, that both measures will return to their new equilibrium levels, with inflation remaining higher and real GDP possibly shrinking.

Weak GDP Growth Data underwhelms when increased government spending and deficits are factored in

The US Department of Commerce ’s “advance” estimate of second-quarter GDP, published on July 27, increased by +2.4% YoY, while Q1 was revised to +2% YoY. Some commentators applauded, calling these readings better than expected and indicators of a resilient economy. In isolation, we agree these numbers are favorable, but looking at the broader economic picture, we take exception to this read. In our view, the reported GDP growth is low quality at best, precisely because it is accompanied by unsustainably high levels of government deficit spending.

Q2 GDP puts the average for the first half of the year at +2.2% (annualized). While the government officially projects a deficit of ~6% of GDP, we expect that reading to be much closer to 8%, with our base case estimate coming in at 7.6%. For a more detailed discussion of the US’s deteriorating fiscal picture, please review our June report.

Historically, the Federal budget deficit has been around 3% of GDP. If the government were to attempt to reach that reading now, either by higher taxes or lower spending, the result would almost certainly be negative GDP growth and a recession. To reiterate our call from June, absent significantly increased government spending, the US economy would have already been in a recession.

Of course, borrowing money only to spend it does not actually create additional economic value, but can provide enough short-term spending power and stimulus to temporarily inflate GDP. In the longer term, however, there is a cost for deficit spending today that comes in the form of a higher cost of debt in the future and, therefore, a worsening trade-off for the government between growth and inflation.

We believe the current level of government spending, especially if it remains unaccompanied by a major improvement in productivity, will significantly damage the future economic prospects of the United States.

The fiscal picture in the US continues to deteriorate justifying a Fitch downgrade

Given this background, we see the Fitch downgrade of United States ’ credit rating as entirely justified. Over the past 4 years, the size and scope of Federal government spending, including on Covid relief programs, has significantly increased while the

accompanying growth in GDP has been anemic at best. As a result, the Debt-to-GDP ratio for the United States has moved to an unsustainable trajectory.

In response to the Fitch downgrade, Secretary of the Treasury Janet L. Yellen released a statement saying that “The change by Fitch Ratings announced today is arbitrary and based on outdated data.” In this case, we find ourselves in rare agreement with Secretary Yellen, as we also believe that Fitch is using outdated data. The implication of this outdated data is, in our view, that their downgrade relied on inputs that were too optimistic. For example, Fitch expects the government deficit to rise to 6.3% of GDP in 2023, whereas our base case is 7.6%. Indeed, we also take exception to Fitch’s assignment of a Stable Outlook to the Federal government’s credit rating.

We do, however, agree with Fitch’s view that confidence in Congress’s fiscal management has eroded. In our view, the June bipartisan agreement to suspend the debt limit until January 2025 is a clear example of a failure to meaningfully manage the federal budget. Despite much fanfare, the legislation was inconsequential in reducing deficit spending or creating policy frameworks for managing the budget going forward. Moreover, the funding of war in Ukraine is likely to exert additional budgetary pressure over an indeterminate number of coming months.

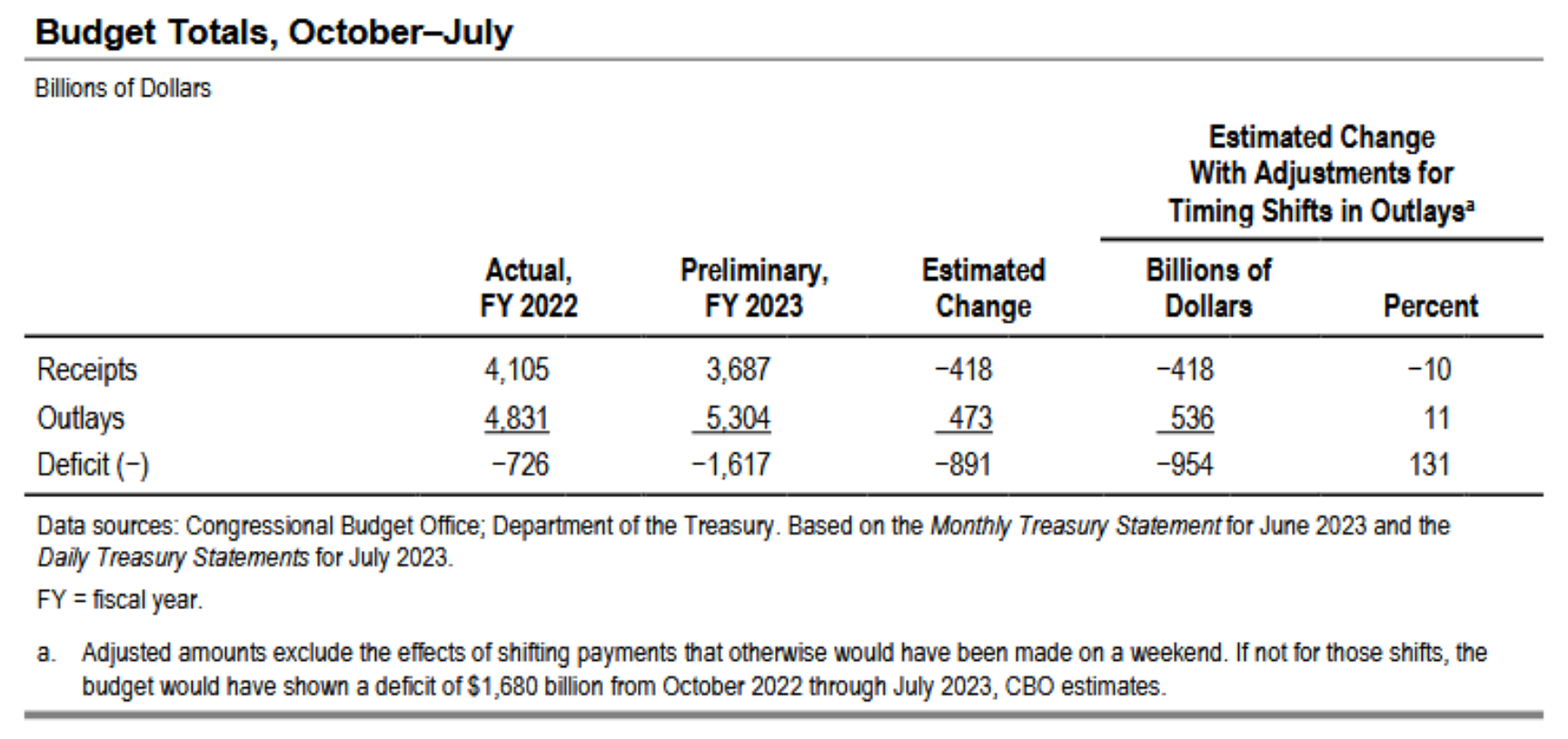

To illustrate this, please take note of Figure 2, which shows revenues that are worse than last year and are accompanied by growing outlays.

At its current pace, the deficit will quite easily surpass the $2 trillion mark before fiscal year end. As a case in point, July’s deficit number includes $69 billion outlay related to implementing income-driven student loan repayment plans. These new “modifications” are separate and distinct from the debt cancellation plan previously prohibited by the Supreme Court. We anticipate several additional expense and spending “surprises” to surface in the current fiscal year, especially as figures in Washington generally find spending money guided by election polling to be more straightforward than managing budgets based on rigorous analysis of economic data. Apparently, there is always a crisis or catastrophe out there that would require expeditious government spending.

In addition to “spot” measures of fiscal distress , such as deficit spending, long-term measures also paint an alarming picture. We believe the Debt-to-GDP ratio is currently ~113% and is likely to get worse. To provide a frame of reference, AAA countries typically have a median Debt-to-GDP of 39.3% and AA countries have a ratio of 44.7%.

We believe the US may soon reach Debt-to-GDP levels of 120%, which would have significant long-term repercussions. For example, higher interest rates would be necessary to control the resulting inflation, thus forcing the government to use a larger portion of its receipts to cover interest expense, resulting in still greater fiscal pressure. Negative feedback loops are perilous, indeed.

The moral to this story may be that a group of politicians voting to spend money will not create more productive capacity in the economy. The result would actually be that the economic system will find its equilibrium through higher inflation and a devaluation of the currency, eventually forcing politicians to actually reduce spending in order to make room for debt service or to choose more nuclear options such as debt restructuring and default.

There is an inconsistency between GDP and GDI numbers, with the latter indicating that we have already entered a recession

We have been vocal about our view that the US economy is headed toward a recession rather than the “soft landing” that a vocal majority seems to be trying to make happen by talking about it with airs of confidence.

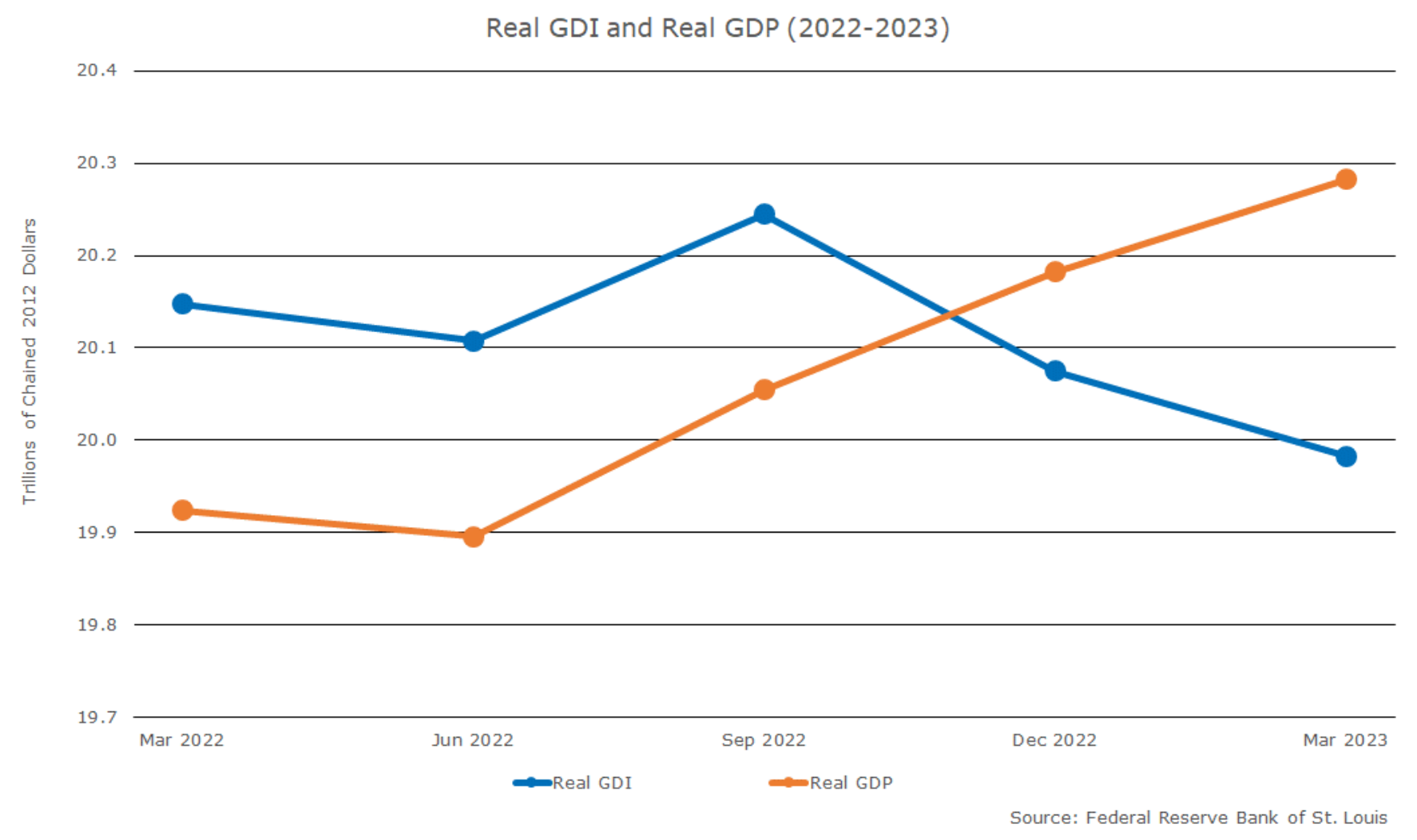

The recently published GDI supports our view by demonstrating a recent contraction. GDP and GDI are two measurements of a country’s economic output . GDP measures the total value of all goods and services produced and is essentially the “output” measure, while GDI measures total income earned by households, businesses, and the government within a country’s border . In principle, GDP and GDI should equal one another because every dollar spent (output) on a good or service flows as income to households, businesses, and the government.

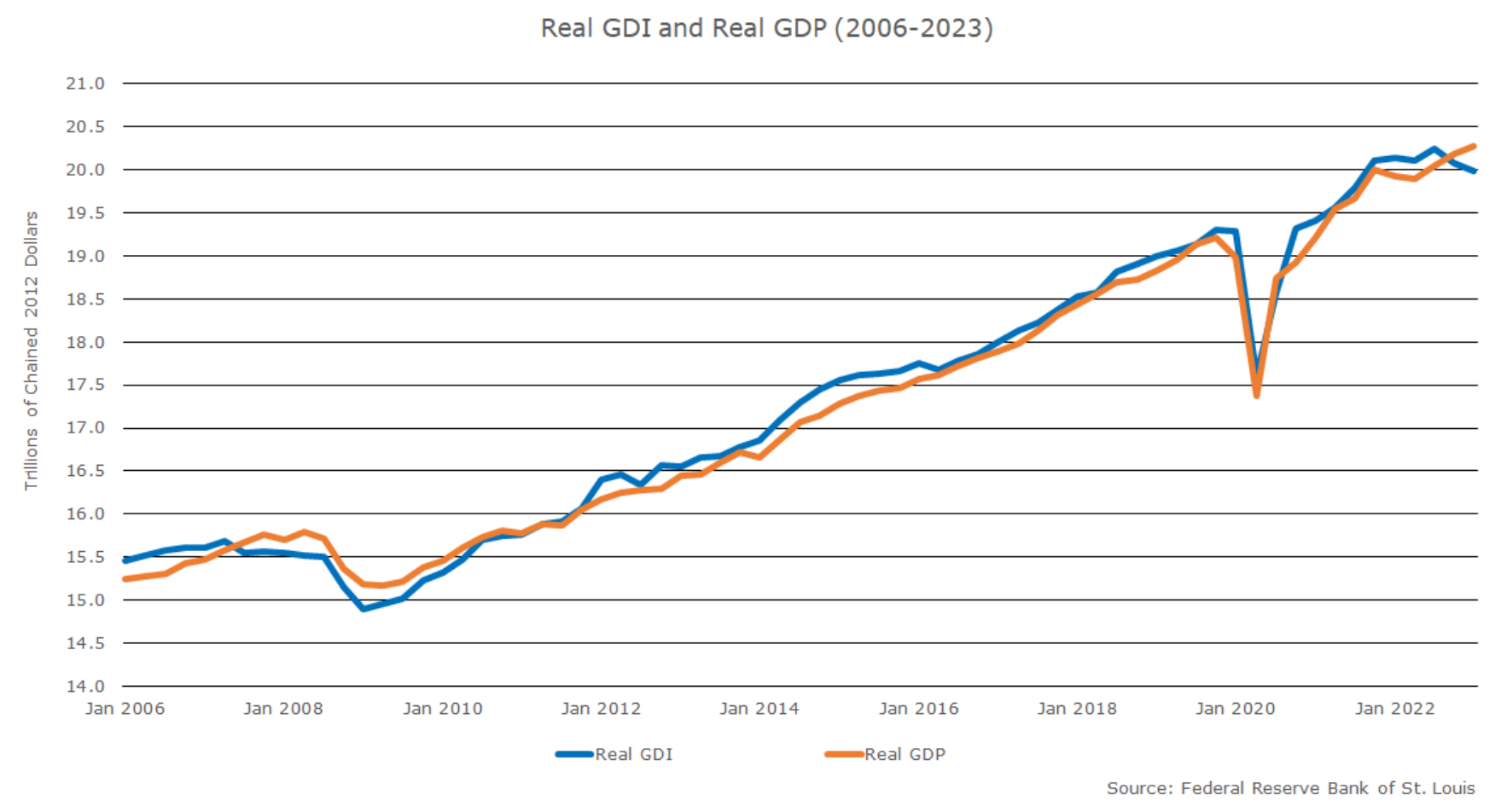

Figure 3 illustrates the historical relationship between GDP and GDI since January 2006. As evidenced, GDI and GDP follow the same trends, with GDI positioned slightly above GDP for most of the observed period. The only exception to this relationship was leading up to and during the Great Recession of 2008.

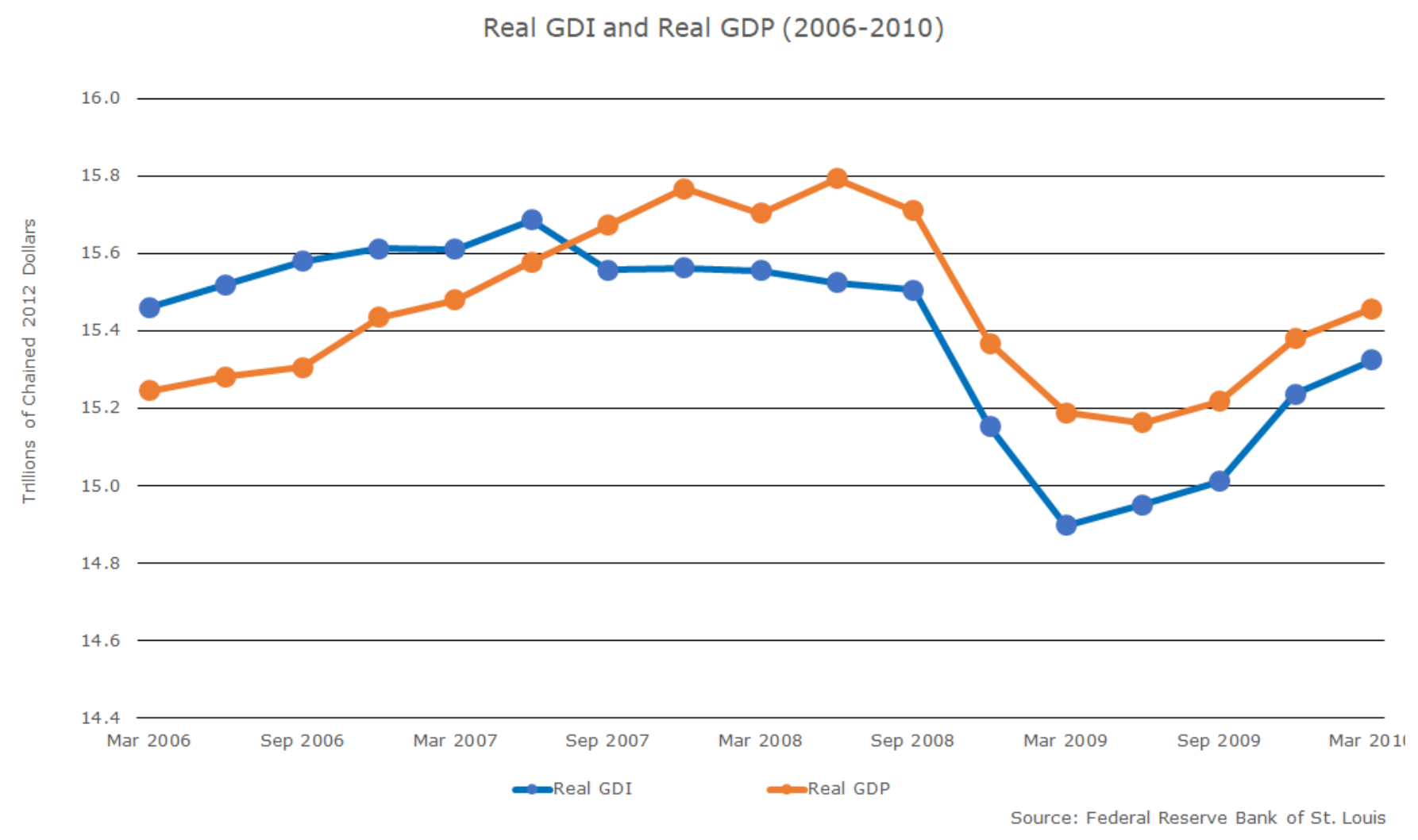

Figure 4 focuses specifically on the relationship between GDI and GDP leading up to and during the Great Recession of 2008. We call your attention to the reversal of positioning in GDI and GDP in 2007 and the maintenance of this positioning until late 2010 (see Figure 3). It is notable that the only time in the observed period GDI was less than GDP was during the Great Recession.

With that said, we now want to highlight the relationship between the two since 2022. In Q4 2022 GDP and GDI crossed, with GDP increasing further in Q1 2023 while GDI declined further during the same period.

According to the Bureau of Economic Analysis, real GDI experienced negative growth BEA shows that real GDP increasing at an annual rate of 2.6% in the fourth quarter of 2022, with a further gain of 2% in Q1 2023 (all numbers seasonally adjusted annual rates).

The ongoing widening of the gap between these two measurements (Figure 5) paints a picture similar to what was observed in the second half of 2007, the period leading up to the Great Recession of 2008 (see Figure 4). We will continue to report on this relationship as new data becomes available.

If GDP were to instead converge to current GDI measurements, we would already be in a " not-so-shallow " recession. It is entirely possible, of course, that GDI numbers could instead converge to GDP measurements. Both scenarios are likely due to data errors resulting from well-known data collection difficulties for both GDI and GDP. In our view, however, the truth likely lies somewhere in the middle.

We would like to point out, however, that while we should consider all economic data while also being aware of the potential for risk measurement errors in any single number, certain economic measures are more substantive, if you will, and thus more difficult to manipulate. We call these data “harder” numbers, and we consider them with greater weight.

We believe that a number of hard measures of economic activity, such as tax receipts, are indeed more in line with the trajectory of GDI. That tax receipts are shrinking — as is GDI — indicate the possibility of recession in at least some sectors of the economy.

Banks’ access to liquidity has improved, but at what cost?

Lastly, we would like to briefly touch on some of the regional bank earnings that were announced in July. Generally speaking, most regional banks and mega-banks reported stable deposit levels, indicating that the recent deposit drama has largely stabilized. It is increasingly evident, however, that the cost of deposits is more elastic than previously assumed and requires banks — even larger ones — to start paying for their deposits.

As recent increases in government debt mean more government securities hitting the open market even as the appetite for foreign buyers to hold US debt diminishes, there will be more competition in this domain and still higher rewards for deposits.

At this point, it is not far-fetched to argue that the government and banks are competing to be the destination people choose for their savings. This dynamic will place pressure on banks ’ balance sheets while simultaneously curbing these institutions’ ability to extend credit or hold assets as the cost to fund these activities with deposits continues to increase.

We expect current market dynamics to continue to create market opportunities for funds like us in the medium term.

Disclosures

The information contained in this document is for informational purposes only and should not be considered investment advice. This document does not constitute an offer to sell, a solicitation of an offer to buy, or a recommendation for any security or investment strategy.

Past performance is not indicative of future results. All investments carry risk, including the possible loss of principal. The views expressed herein are those of the author as of the date of publication and are subject to change without notice.

Forward-looking statements are based on current expectations and assumptions, which are subject to risks and uncertainties. Actual results may differ materially from those anticipated.

Monachil Capital Partners LP is a private investment firm. Investment opportunities described herein may be available only to qualified purchasers as defined under the Investment Company Act of 1940.